On 15 April 2021, the US announced further sanctions against Russia[1]. The Biden administration announced the move on the back of long-discussed claims of cyberattacks, alleged meddling by Russia in the 2020 US presidential elections and alleged bounties offered by Russia to Taliban militants in Afghanistan.

The new sanction measures include:

- US investors being prohibited from purchasing Russian sovereign debt (OFZ) denominated in roubles and issued after 14 June 2021 on the primary market

- Restrictions against 32 individuals and organisations accused of disinformation and interference in US affairs, including the elections.

Russian financial markets have so far appeared resilient to the news, with investors judging that the new measures are not as threatening as they sound. After initially dropping by 2%, the rouble quickly started to correct and returned to its pre-announcement level the following day. Russian bonds and equities also completely recovered. Why is that?

- The new measures do not restrict US investors from purchasing rouble-denominated Russian government bonds on the secondary market

- There is no obligation for US investors who already hold Russian bonds to sell-off their positions.

- It seems that both Russia and the US are still open for dialogue. Investors were initially concerned that the meeting between Presidents Putin and Biden might be cancelled due to increasing tensions. However, as it became apparent later from Biden’s speech, during their telephone call on 13 April he let President Putin know that new sanctions would be imposed. Nevertheless, Putin has agreed to an audience with Biden.

US banks had already been barred from buying Russian sovereign Eurobonds[2] on the primary market since August 2019. There was no material effect on the market from this ban. Russia’s Ministry of Finance managed to place EUR 2 billion of Russian Eurobonds that year without the participation of US investors.

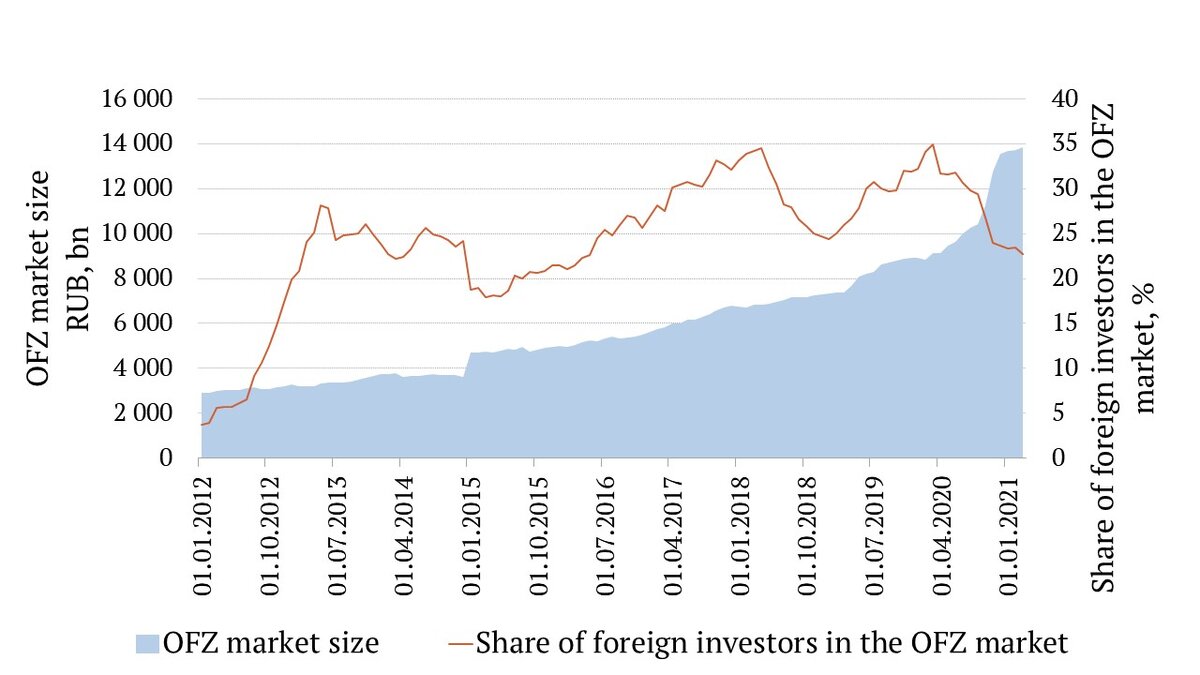

Additionally, sanction fears had already led non-residents to get out of the Russian sovereign debt (OFZ) market. At the beginning of April 2021, the share of all foreign investors in OFZ had fallen to 19.7% from 31.7% a year earlier. Their share of the primary OFZ market was only about 10%. Most of the debt is now financed by Russia’s government-owned banks. Nonetheless, since the beginning of April 2020, the OFZ market volume has risen by 52%, and is now at a record level of RUB 13.9 trillion (~USD 183 billion).

Share of foreign investors in OFZ

Sources: The CBR, TKB Investment Partners

According to the Central Bank of Russia (CBR), at the beginning of the year, US investors’ share of the total OFZ market was only 6.9% or USD 12.8 billion.

As Washington has not convinced the EU or the UK to support the new sanctions, investors from those countries, who hold some 12% of OFZ, can continue purchasing Russian debt with no restrictions.

What was Russia’s response?

The Ministry of Finance and the CBR have announced the following measures to minimise the effect of the new sanctions on the Russian market:

- Internal government borrowings will be reduced by USD 12 billion (RUB 875 billion). Instead, free funds from the federal treasury will be used

- Decisions about the upcoming OFZ auctions will be made with regard to the market dynamics

After 14 June, the Ministry of Finance will place only new OFZ. There will be no additional placement of existing government bonds.

Authors: Vladimir Tsuprov, CIO; Aleksandra Kuznetsova, Investment Specialist; Marina Tsutskiridze, Investment Specialist

[1] The White House statement

[2] Flashnote: The second round of Skripal case related sanctions from the US (November 2019)