Russia is much better prepared for a drop in oil prices now than it was in 2014, 2008 or 1998. There is no currency targeting, net debt is close to zero, budget is in a surplus and budget rule protects Russia from oil price drop all the way down to USD 42 bbl level. This is the first time in the midst of a significant drop in oil prices that the yield on Russian Eurobonds denominated in US dollars has risen slightly. There has only been a 30bp rise in Russian state Eurobond yields to maturity since the end of last week (1).

Russian equity market fundamentals have not deteriorated materially on the back of the recent oil price drop. Expected average dividend yields are in double-digit figures. Expected inflation is around 4% even allowing for the impact from rouble depreciation since the start of the year. This leaves the Central Bank of Russia (CBR) room for key rate cuts over the next two to three years.

USD 40/bbl is a fundamental bottom price for Brent crude

US shale oil producers are likely to follow OPEC+ in terms of reducing oil production output. The US produces 7.4 million barrels of shale oil per day. It appears that current WTI prices of USD 33-35/bbl are below the breakeven level for 30%-40% of existing wells and below the price needed to profitably start 90%-95% of potential new wells. With current oil prices, US shale oil production is likely to drop by 2-3 million barrels per day over the coming 12-24 months.

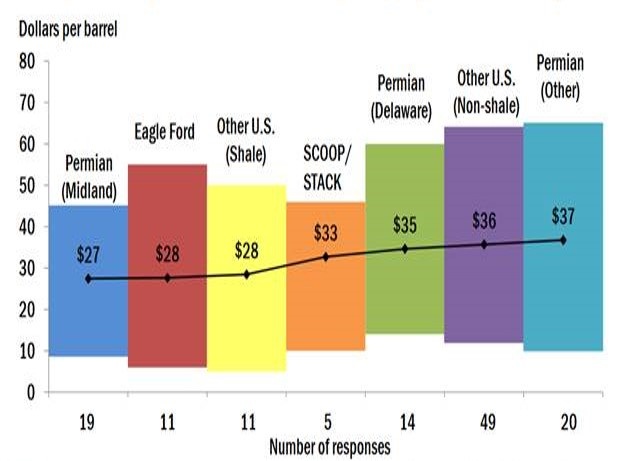

Shut-in prices for existing wells

Dallas Fed Energy Survey – In the top two areas in which your firm is active: What WTI oil price does your firm need to cover operating expenses for existing wells?

Notes: Line shows the mean, and bars show the range of responses 87 E&P firms answered this question from March 13-21, 2019.

Sources: Federal Reserve Bank of Dallas.

Breakeven prices for new wells

Dallas Fed Energy Survey – In the top of two areas in which your firm is active: What WTI oil price does your firm need to profitably drill a new well?

Notes: Line shows the mean, and bars show the range of responses 82 E&P firms answered this question from March 13-21, 2019.

Sources: Federal Reserve Bank of Dallas.

The adverse impact of the coronavirus outbreak on global markets could be short-lived. The key concern is that there will be not enough medical resources to treat patients should the virus affect very large numbers. However, China and South Korea are demonstrating that it is possible to curb the spread of the virus.

Sources: ECDC, World Health Organisation, TKB Investment Partners

Hong Kong is also showing that it is possible to prevent the virus from spreading exponentially.

Sources: ECDC, World Health Organisation, TKB Investment Partners

Should there be news of a treatment that could at least limit the mortality rate to that of the ordinary flu, the situation would markedly improve.

Oil war between Russia and OPEC can end unexpectedly. It appears that the failure of OPEC+ to agree a deal for further production cuts revolves around member countries not wanting to continue losing market share to US shale oil producers. Should oil prices remain stuck at their current level for a prolonged period, it could put the agreement back on the table as a way of pushing the price up to the range of USD 40-50/bbl, at which point it would still be hard for US companies to increase production.

Market outlook

Russia’s economy is well prepared for the current turmoil, as we wrote in November last year. Net government and corporate debt is close to zero. The budget and current account are in surplus. The budget rule has helped significantly to limit the impact of lower oil prices on the rouble. In response to the 19% drop in oil price (2) since the end of last week, the rouble has weakened by only 4% (3). The overall 13% depreciation of the rouble (4) over the year to date is likely to add 1% to the inflation forecast for this year, taking it to 4% from 3%. Four per cent is the CBR’s long-term inflation target. Inflation at 4% means the real yield on the Russian bond market is now around 3%. This should materially limit the risk of profit-taking by international investors in this market, thereby much reducing the risk of further pressure on the rouble.

The expected average dividend yield for the market is now at double-digit levels after the recent drop in share prices. It remains the highest among emerging equity market average yields.

With the current spike in volatility on financial markets, the CBR is likely to pause its rate cutting. However, over the next one to three years, there is still room for key rate cuts if inflation is at around 4%.

Speed-boost options related to surprises on GDP growth side have become less likely. With oil prices probably remaining in a lower range over the next one to three years, it is likely to put tighter limits on the funding of infrastructure investments.

(1), (2), (3), (4) Figures as at the end of 10 March 2020

Authors: Vladimir Tsuprov, CIO and Egor Kiselev, Head of International Business & Investment Marketing