Russian equity market dynamics

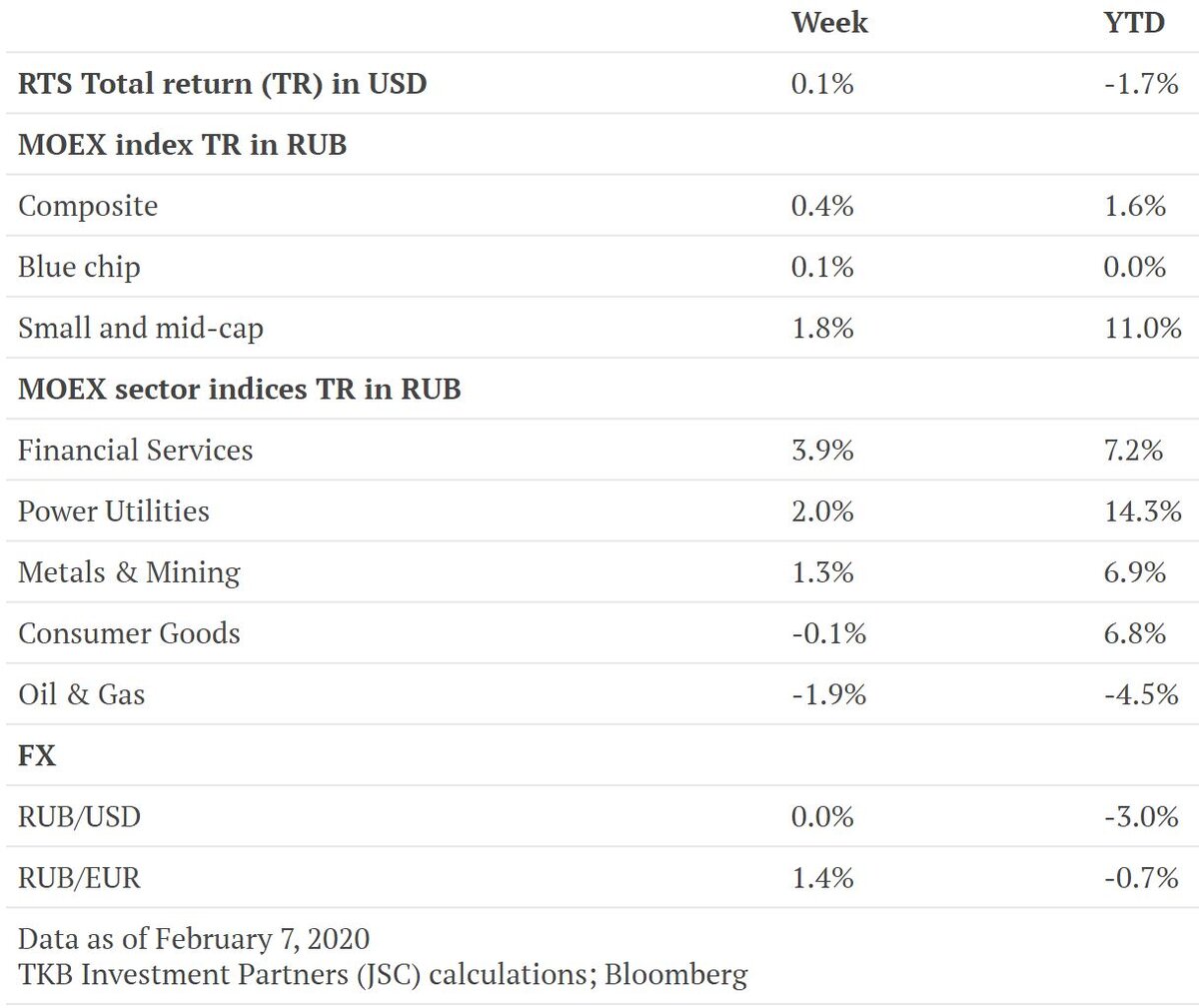

Last week, the Russian equity market grew slower than the other emerging markets (EM). The RTS index gained 0.1%, while the MSCI EM index rose by 2.8% (all figures in USD terms). Broader EMs were positively affected by news of progress with vaccines against Coronavirus. China reducing tariffs on US imports also lifted investor optimism. Stock-specific factors troubling the benchmark heavyweights put pressure on the Russian market. As the 25bp rate cut by the Central Bank of Russia was widely expected, it had no impact on the Russian market.

The financial sector outperformed the broader market, mainly driven by TCS and VTB, whose shares rose by 9.7% and 3.6%, in rouble terms, respectively. Both companies rose despite the lack of fundamental news.

The oil & gas sector lagged the wider market. The worst performers were Novatek and Rosneft. Novatek reacted slower than its peers to falling gas prices. Rosneft’s share price was hit by the report from BP, which indicated that Rosneft’s revenues fell in Q4 2019, and by news that the US was considering imposing sanctions on the company because of its ties with Venezuela. The likelihood of material sanctions happening is low, in our view. According to Bloomberg, US Treasury Department officials are concerned that new sanctions against Rosneft would cause chaos in the oil market and raise prices given that Rosneft currently extracts approximately 5% of global oil.

Main Russian news

Inflation in Russia continued to slow in January. Consumer price inflation (CPI) slipped to 2.4% YoY at the end of January from 3.0% YoY at the end of December. Inflation slowed in the food, non-food and services sectors. Food inflation slipped to 2.0% YoY from 2.6%, while non-food inflation contracted to 2.5% YoY vs. 3.0%. Services inflation slowed to 2.8% YoY from 3.8%. The Central Bank of Russia (CBR) forecasts inflation will be 3.5%-4% by the end of 2020, which is close to its target of 4%.

The CBR cut its key rate by 25bp to 6%, the sixth consecutive cut it has made. The cumulative effect is expected to take place in the second half of 2020. The main reasons given for the cut were slowing inflation, uncertainty in industrial production and weak demand. CBR governor, E. Nabiullina, hinted of the possibility of another cut at the next meeting in March 2020, although this is not certain. While the CBR left unchanged the neutral rate range with the lower bound of 6%, Mr Nabiullina claimed the CBR is ready to consider lowering this range.

Russia’s economy grew by 1.3% in 2019, according to Rosstat. This was in line with the Ministry of the Economic Development’s forecast. The main contributors to GDP growth were the financial, extraction and hospitality sectors. For the first time since 2009, exports declined, with analysts citing as the main reasons the trade war between China and the US and lower oil exports. The Ministry of Economic Development upgraded its 2020 GDP growth forecast to 1.9% from 1.7%. Its expectations for 2021 GDP growth remained the same, at 3.1%.

To watch…

There is no significant news to follow this week.

Author: Aleksandra Kuznetsova, Junior Investment Specialist

Sources: Rosstat, Bloomberg, TKB Investment Partners (JSC); February 2020