Russian equity market dynamics

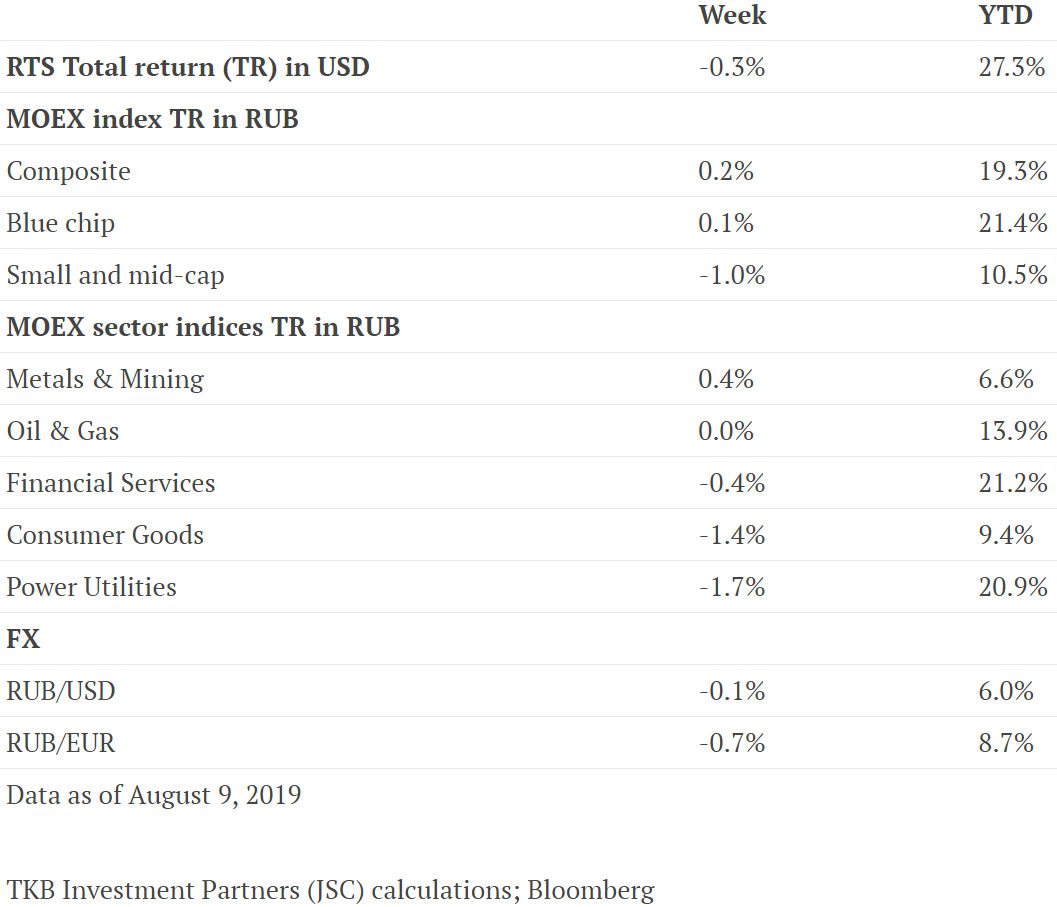

Last week, the Russian equity market contracted, although by less than the broader emerging markets (EM). The RTS index lost 0.3% while MSCI EM index lost 2.2% (all figures in USD terms). It appears that that strong value characteristics helped Russian equities escape most of the pressure on EM overall. Even a 5.2% fall in oil prices over the week failed to have any significant impact on the Russian market.

The metals & mining sector was the best performer, mainly due to Polyus and Polymetal, whose share prices rose by 7.7% and 6.8%, respectively, in rouble terms. This was on the back of news about the trade relationship between the US and China, and increased expectations of a US rate cut, which boosted gold prices.

The power utilities sector was the worst performer of the week, dragged down mainly by Rosseti and Inter RAO. There was no news to justify the poor performance of these stocks.

Main Russian news

Inflation in Russia is continuing to slow. The consumer price index (CPI) slipped to 4.6% YoY as at the end of July from 4.7% YoY at the end of June, mainly due to lower services sector inflation, which fell to 4.5% YoY vs. 4.9% YoY. Food inflation remained at 5.5% YoY, as in June. Non-food inflation rose slightly to 3.6% YoY vs. 3.5% YoY. The July inflation print means it is already within the Central Bank of Russia’s target boundaries for 2019 (4.2%-4.7%).

The S&P rating agency claimed that the latest US sanctions are no threat to Russia,saying that they will have no immediate impact on Russia’s investment grade credit rating. The agency added that even the ban on all primary sovereign debt should be tolerable in view of the Russian government’s strong balance sheet and its limited borrowing needs. The government’s 2019 debt issuance plan has already been achieved. In 2020-2021 Russian government announced a low borrowing bar of only USD 3 billion a year. Most of the debt is issued in roubles. As the new US sanctions do not cover such borrowings, their effectiveness will be limited.

Fitch rating agency upgraded Russia’s rating to BBB. Since 2017, it had rated the country BBB-. The agency explained the upgrade by saying that Russia has achieved a stronger policy mix which has resulted in macroeconomic stability. It emphasised Russia’s sensible tax policies, commitment to its inflation target and its robust external balance.

To watch…

Rosstat is due to post preliminary Q2 2019 GDP figures.

Author: Aleksandra Kuznetsova, Junior Investment Specialist

Sources: Vedomosti, Rosstat, Bloomberg, TKB Investment Partners (JSC); August 2019