On 1 August 2019, the US imposed new sanctions against Russia. It was the 54th time that new sanctions from the US and the EU have been brought to bear since March 2014. Over 1-2 August, Russian equities contracted by 5.7% vs. a 3.2% drop in the MSCI EM index (all figures in US dollar terms).

Is the latest round of sanctions a game-changer for Russia?

Details

- US banks will not be able to buy hard currency-denominated Russian sovereign debt on a primary market or lend in hard currency to Russian sovereign institutions

- The US will oppose financial or technical assistance to Russia from international financial institutions

- Export licensing restrictions imposed.

Links to official documents: press statement, executive order, directive.

Why?

Skripal poisoning case[1]. The UK suspects that two Russian citizens were involved.

In August 2018, the US imposed a first round of sanctions related to the Skripal case. Initially the plan was that a second round of sanctions would be put in place in November 2018.

How big a potential impact on the Russian economy?

The new sanctions will likely have only a very minor effect:

- External financing is not crucial for the Russia budget. The country’s external state debt equates to 3% of GDP. Overall, Russia’s state debt-to-GDP ratio is 14% – the lowest among the top-20 largest countries in the world

- US banks can continue buying any Russian hard currency state debt on the secondary market

- US banks can continue operations with Russian rouble-denominated state debt on the primary and secondary markets

- Russia is in no need of technical or financial assistance from international financial organisations

- Export licensing restrictions do not add new limitations on the export of goods and services to Russia from the US, which are crucial for the Russian economy.

Previous sanctions

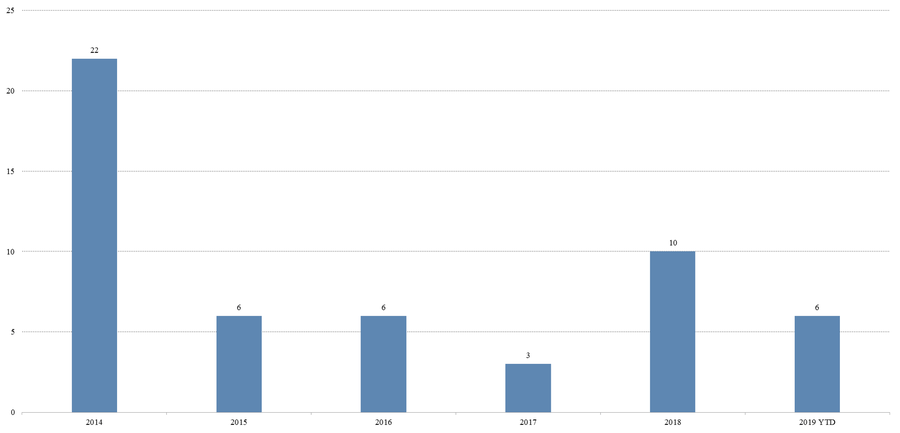

Despite 53 sanctions actions on Russia from the US and the EU between the end of February 2014 and the end of July 2019, Russia’s equity market has outperformed broader EM equities on average over this period.

Even with a 41% drop in oil prices, Russian equities have proved highly resilient.

Reasons:

- The sanctions have a very small impact on the Russian economy

- The Central Bank of Russia (CBR) and Ministry of Finance significantly limited the adverse impact of the lower oil prices

- Many listed Russian companies have strong fundamentals.

Number of sanction actions against Russia from the US and the EU

YTD – as at 31 July 2019

Sources: RadioFreeEurope, Vedomosti, TKB Investment Partners, August 2019

Largest EM equity markets’ performance: March 2014- July 2019

Sources: Bloomberg, TKB Investment Partners, August 2019

Why is the US still imposing fairly weak sanctions?

Any material sanctions are likely to have a dramatic boomerang effect. The Russian economy is significantly integrated into the global one:

- Russia is the second largest net oil exporter in the world

Net crude oil export in 2018, mn tonnes

Sources: BP, TKB Investment Partners, August 2019

- Russia is the largest external gas supplier to Europe

Share of 2018 gas exports to Europe

Sources: BP, TKB Investment Partners, August 2019

- Russia is one of the top 20 largest countries in terms of international trade volumes.

International trade volume in 2018, billion US dollars

Sources: WTO, TKB Investment Partners, August 2019

Authors: Egor Kiselev, Head of International Business & Investment Marketing and Gennady Sukhanov, Head of Research & Deputy Head of Equities