Russian equity market dynamics

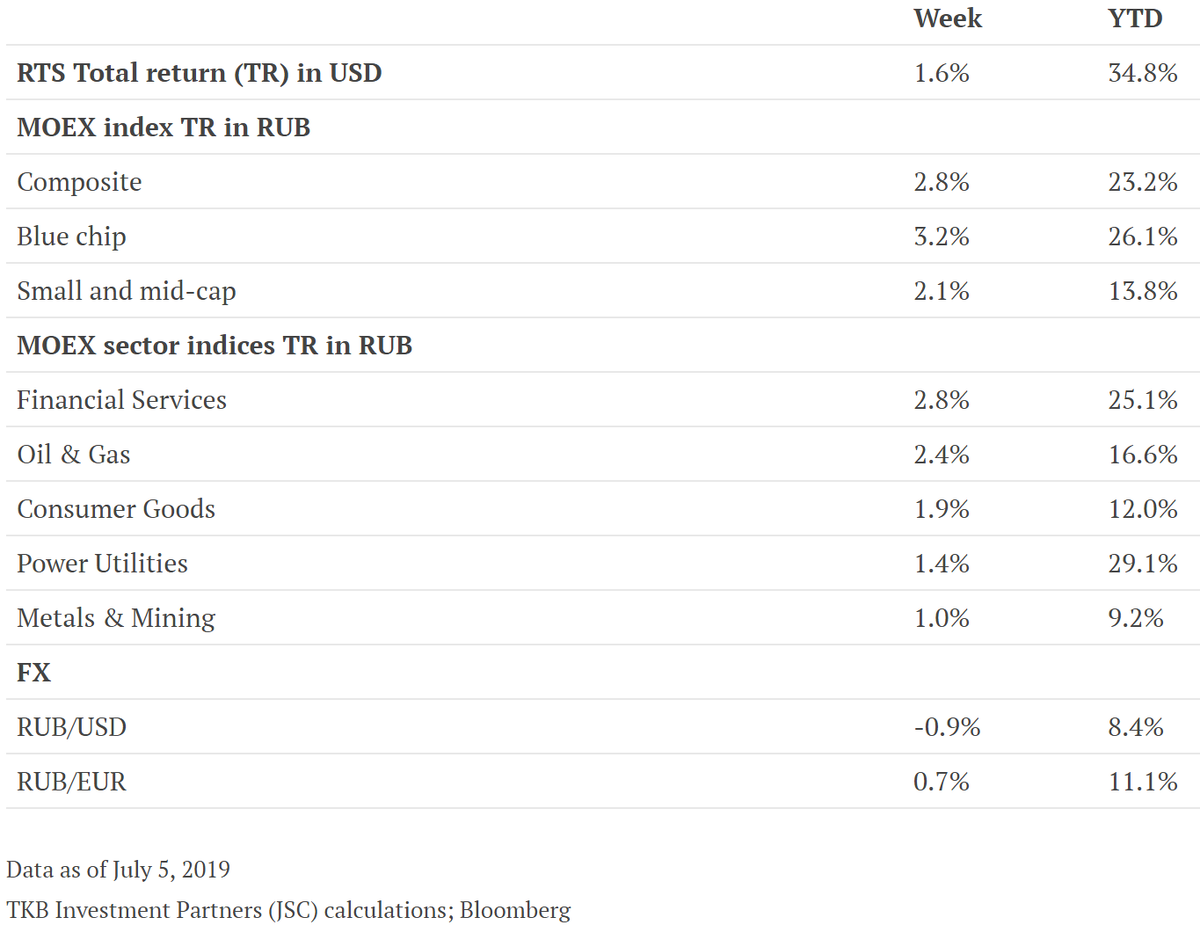

Last week, the Russian equity market outperformed other emerging markets (EM). The RTS and MSCI EM indices rose by 1.6% and 0.7%, respectively. Russia was the third best performing market among EMs. This is possibly due to the central bank (CBR) dropping hints about further interest rate cuts. At the same time, global markets were on hold, waiting for the latest US labour market statistics to be published.

The financial services sector outperformed the market. This was mainly due to Moscow Exchange, which rose by 5.6%, Sberbank, with a 1.8% increase, and VTB, which increased by 3.7% (all figures in rouble terms). Moscow Exchange published its trading update for June. The growth leaders were equity, +38.4%YoY, and the bond market, with a 13.6%YoY increase, both in rouble terms. Sberbank published its Q2 RAS report, showing a 8.8% YoY increase in earnings. VTB rose despite the lack of fundamental market-moving news.

The metals & mining sector was the worst performer of the week. It was dragged down mainly by Severstal. The company, which belongs to A. Mordashov, acquired a 26% stake in its joint venture with Germany’s Linde from Power Machines, which is also owned by Mordashov. Originally, Power Machines owned 50% of the joint venture. After US sanctions against the company, its share fell to 26%. This deal potentially increases the sanctions risks for the venture.

Main Russian news

The CBR is considering another 25bp key rate cut. Governor E. Nabiullina, hinted that the bank was planning to lower the key rate to 7.25% at its July meeting. Nabiullina emphasised that the CBR will continue with its practice of smaller cuts. We believe a 50bp cut cannot be excluded. She also noted that the inflation outlook was moderate for the next 6-12 months.

Ms Nabiullina talked about possible scenarios for the use of the proceeds of the National Wealth Fund (NWF). According to the Ministry of Finance, the NWF is expected to reach 7% of GDP, which is the threshold for reinvestment, at the end of this year. In Nabiullina’s view, the worst option is to invest all the excess money straight away. This would make the financial parameters and the rouble more dependent on oil price fluctuations. Another option is to invest only part of the excess money, which implies less risks for macroeconomic stability.

OPEC+ agreed to extend the oil production cuts until March 2020. The cuts are running at about 1.2 million barrels per day. The Russian Energy Minister said that the agreement was designed to prevent major volatility in the market. In his view, it was not right to make any sudden changes now. Despite the lower output, crude oil has fallen from a six-month high in April (above USD 75 a barrel) to below USD 63 this week. The pressure is coming from market concerns over slowing economy growth.

To watch…

Rosstat is due to publish the consumer price index (CPI) report for June. CBR is to report its estimate of the BoP for Q1 2019.

Author: Aleksandra Kuznetsova, Junior Investment Specialist

Sources: Vedomosti, Rosstat, Bloomberg, TKB Investment Partners (JSC); July 2019