Russian equity market dynamics

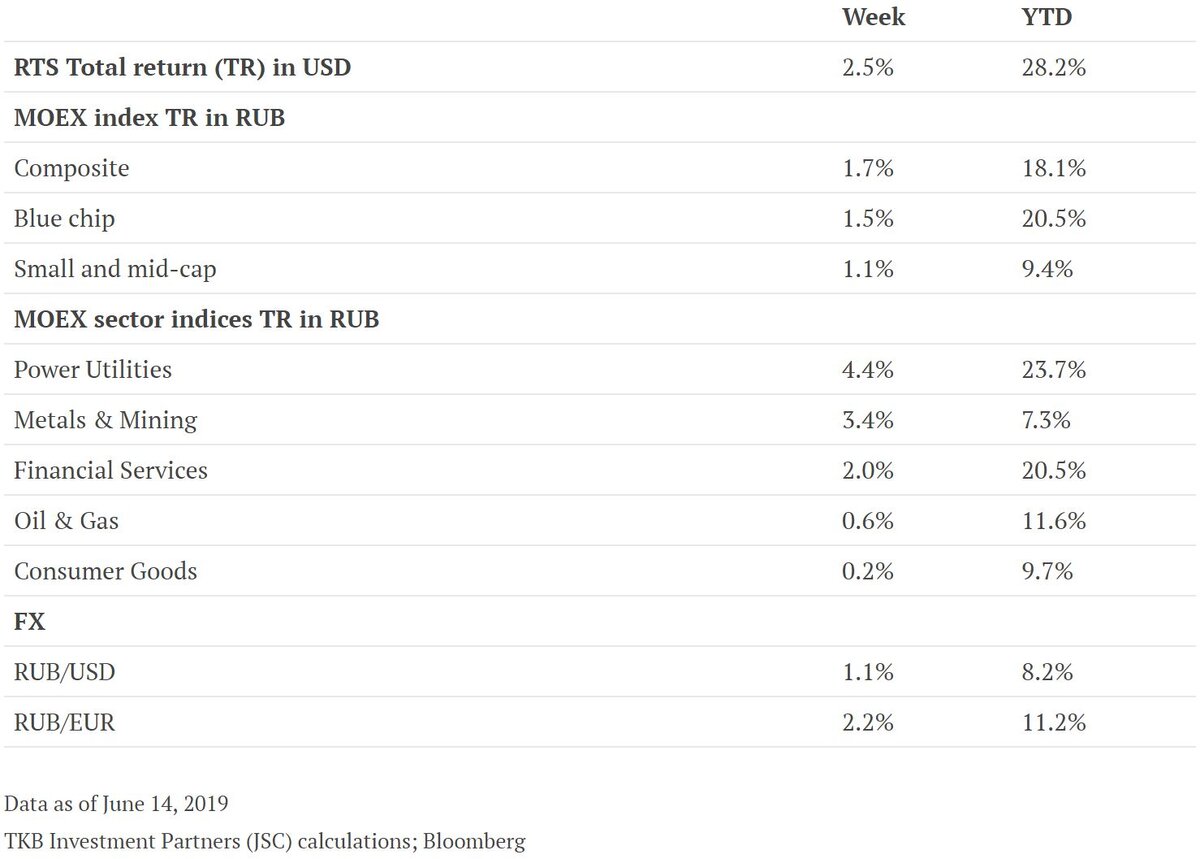

Last week the Russian equity market continued to outperform emerging markets (EM). RTS and the MSCI EM index rose by 2.5% and 0.9% respectively in USD terms. The overall rise of EM was due to chance of softer monetary policy from central banks around the world, particularly the Fed. The Russian Central Bank deciding to cut the key rate by 25bp helped the Russian market to outperform its EM peers.

The power utilities sector outperformed the market. This was mainly due to Inter Rao, whose shares increased by 8.9% in rouble terms. There were no significant news or events to explain the strong performance of this stock.

The consumer goods sector was the worst performing sector of the week. It was dragged down mainly by RosAgro, despite the lack of any significant explanations to justify the poor performance of the stock.

Main Russian news

The Central Bank of Russia (CBR) has cut the key rate by 25bp to 7.50%. The main reasons are the following: 1) a fall in the short-term inflation risks, 2) lower than anticipated inflation and 3) greater stability of the rouble. Since February, monthly inflation rates have been around 4% in annual terms adjusted for seasonality. Overall inflation in annual terms has been contracting. As of 10 June it was 5.0%. CBR hinted that a further reduction of the key rate is possible later on this year; intending to cut the key rate to a neutral level of 6-7% by mid-2020. The new risk for this scenario concerning how to use funds of the National Wealth Fund is currently being discussed. The fund is likely to reach 7% of GDP by the end of the year. The part of the fund in excess of the 7% level can be used for investments in the Russian economy.

US has drafted a bill to sanction work on the Nord Stream 2 pipeline. Bill’s target is the Nord Stream 2 pipeline that would take natural gas from Russia to Germany. The sanction draft targets vessels that lay the pipeline and denies visas to executives from companies linked to those vessels. The Nord Stream 2 is a joint venture of Russian Gazprom and five European energy majors. The deal is exclusively commercial in nature, according to Foreign Minister of Russia S. Lavrov. At present, 58.7% of the total length of the pipeline has already been constructed.

Deputy Finance Minister V. Kolychev stated that foreign investors are now less concerned about risks connected to the US sanctions. Russia attracted RUB 375bn (USD 5.8bn) in May. The Ministry of Finance finished its plan for financing in the first two quarters of 2019, thus it may reduce the OFZ offer for the next half of the year. Kolychev stated that the Ministry of Finance has no strong need for debt financing.

To watch…

Rosstat is due to post the components of GDP in Q1 2019 and key macroeconomic figures for May 2019.

Author: Aleksandra Kuznetsova, Junior Investment Specialist

Sources: Vedomosti, Rosstat, Bloomberg, TKB Investment Partners (JSC); June 2019