Russian equity market dynamics

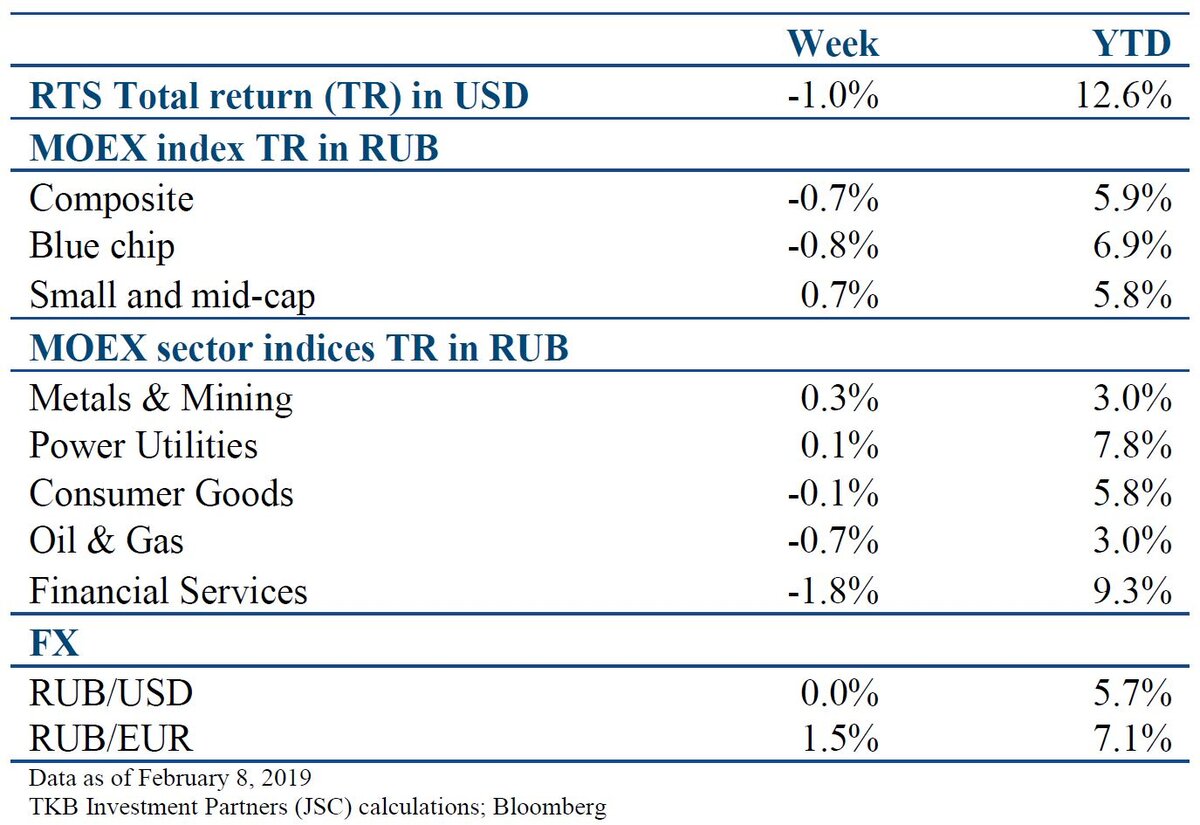

After five consecutive weeks of growth, the Russian equity market has somewhat corrected. Globally, investors were most likely fixing their profits after a healthy year-to-date performance. The MSCI EM and the MSCI World indices slipped 1.3% and 0.4% respectively in US dollar terms, while rising by 7.3% and 7.4% since the beginning of the year. Oil markets followed global sentiments last week and price for Brent crude fell by 1.1% in US dollar terms.

The metal and mining sector was ahead of the market. The leader was Rusal, whose share price rose by 7.6% in rouble terms. The company published operational results for 2018, which indicated an increase in production of aluminum by 1.3%. Meanwhile in January, the US Treasury also lifted sanctions against the company, which were imposed in April 2018. It is likely that this continued to have a positive effect on the stock.

Companies from the financial sector lagged, while outperforming other sectoral indices year-to-date. Stocks of Moscow Exchange and Sberbank were subject to the greatest falls, of 3.0% and 2.7% respectively.

Main Russian news

Inflation has reached 5% YoY in January 2019 from 4.3% YoY in December 2018. Both an increase of VAT and adjustments of prices to rouble weakening in the second half of 2018 contributed to the price growth. Food inflation saw the greatest rise, accelerating to 5.5% YoY from 4.7% YoY. According to the CBR, food inflation largely recovered from its drop in 2017 and the first half of 2018. Non-food and service inflation reached 4.5% and 5.0% respectively, compared to 4.1% and 3.9% in December. Overall, the Central Bank has not changed its inflation forecast: it could reach 5%-5.5% in 2019 and decelerate to 4% in the first half of 2020.

The Central Bank of Russia maintained its key rate at 7.75%. This decision was based on the following factors:

- The inflation figure of 5% in January was at the lower bound of the Bank of Russia’s expectations. The CBR estimated that an increase in VAT had a rather moderate impact on the price growth, and that the full effect would not be seen before April.

- Monetary factors remained relatively stable. OFZ yields contracted as global financial markets stabilised, while deposit and credit market rates somewhat increased. Overall, real yields remained positive, supporting saving pattern of consumer behavior.

- CBR’s assessment of pro-inflation risks remained almost unchanged. The most significant uncertainty is stemming from the effect of a VAT increase on prices and the volatility of oil prices: the risk of the supply glut in 2019 remained high. Risks related to wage movements, budget expenditures and possible changes in consumer behavior remained moderate. Meanwhile, the CBR stated that the risk of persistent capital outflow from emerging markets had reduced, as investors are not expecting aggressive rate hikes by the US Federal Reserve and other Central Banks this year.

Moody’s upgraded Russia’s rating to investment grade Baa3, from speculative grade Ba1. The outlook was changed from positive to stable. Moody’s was the last agency* to keep Russia’s rating at the speculative grade. Overall, the agency noted that:

- This upgrade was thanks to government policies that helped to strengthen Russia’s internal and external metrics and make the economy less vulnerable to external shocks (incl. sanctions)

- The low level of sovereign debt, strong state balance and accumulated reserves are likely to provide the country with stability regardless of the structural challenges it faces

- The central bank's foreign exchange reserves currently cover 80% of external debt (including direct investment), compared to 57% coverage in June 2014. Moreover, the capital outflows last year, including net external payments, were more than covered by the current account surplus. The surplus widened to USD 115 bln in 2018 from USD 33 bln in 2017.

- The adoption of pension reforms should support fiscal strength in the long term.

The statement is referred to Big-3 rating agencies: Moody’s, Fitch and S&P.

Author: Maria Rybina, Investment specialist

To watch...

Yandex is due to publish financial results for Q4 and full year 2018

Sources: Vedomosti, Rosstat, cbr.ru, Bloomberg, TKB Investment Partners (JSC); February 2019