Russian equity market dynamics

The Russian equity market continued to rise, along with other emerging markets: the MSCI EM index also gained 1.4% in US dollar terms over the week. In contrast, MSCI World rose only marginally by 0.1%. Overall, as of 23 January, emerging markets equities saw an inflow of USD 3.1 bln, which was a second consecutive week of inflows above USD 3bln. Among that, net inflow into the Russian market over the most recent week was USD 135 mln, mainly through the GEM-funds.

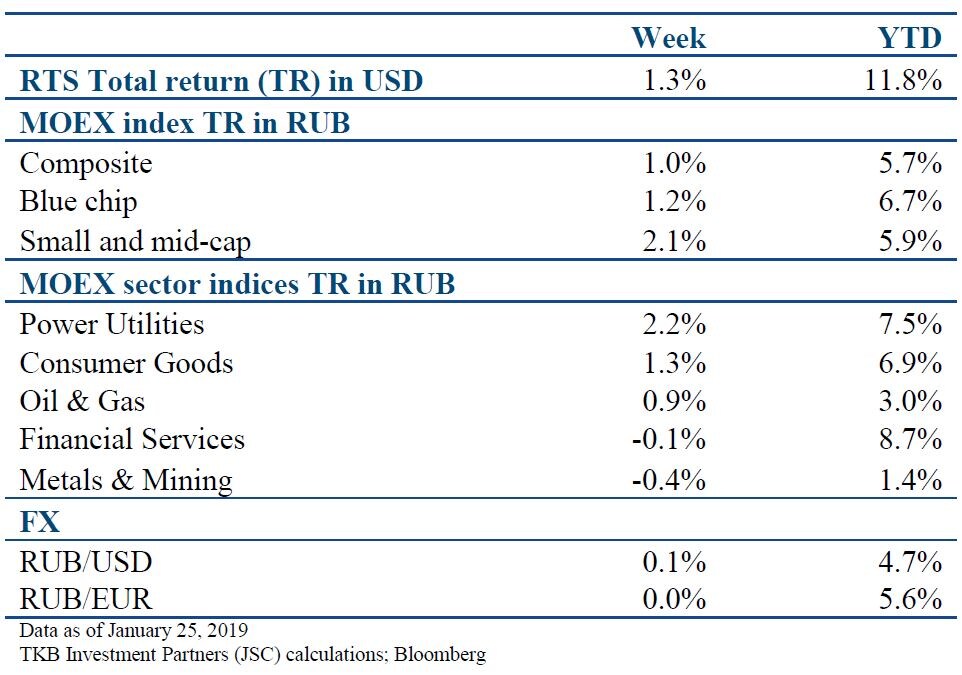

Power utility companies outperformed other sectoral indices. Stronger rouble year-to-date likely continued to contribute to demand for stocks of domestic-oriented companies. Rosseti, Federal Grid and Unipro were the top-performers, with their stocks rising by 9.0%, 5.2% and 2.6% respectively in rouble terms.

The metals and mining sector underperformed for the second week in a row. Alrosa, NLMK and Severstal performed the worst within the sector, with their share prices falling by 2.8%, 2.2% and 0.4% respectively in rouble terms.

Main Russian news

Russian macroeconomic indicators were generally stronger in 2018 compared to 2017. Growth of industrial production was mainly driven by an increase in extraction of mineral resources: Russian coal and oil output rose by 7% and 1.7% respectively compared to an increase in coal production by c. 6.4% and decline in oil output by c. 0.3% in 2017. Growth of consumer demand also accelerated in 2018 driven by both food and non-food segments. This was partly due to notable increase in real wages and partly to a planned increase in VAT that likely resulted in consumer’s early purchasing of non-food items, which explains a more notable growth in this segment.

In 2019, the Russian government will spend RUB 2.2 trl (around USD 33bln) on infrastructure projects, 8.9% more than 2018. These expenses include both traditional expenditures of federal and regional budgets on renovation and expansion, as well as investments in national projects. The latter are mentioned in “May orders” of Vladimir Putin and needed to drive share of investments to GDP up to 25% from the current 21%. According to InfraOne, a Russian direct investment firm, this is not the substantial growth of infrastructure investments needed to fulfil the “May orders”: government’s expenses on infrastructure related to GDP in 2019 could stay flat compared to last year’s 2.1%. There are three main obstacles for investment growth:

- Lack of investment projects, which are ready to be financed

- Capacity limits over the next two years due to limited number of companies in the construction industry. Currently, construction companies can manage projects of around RUB 2.8 bln overall

- Delay in project realisation. Contractor companies might miss the deadlines for a project completion, in case they face a shortfall in funding due to an increase in VAT. The prices in the contracts, which were awarded in 2018 or before, were based on VAT at 18%. As there are a number of projects which will last for several years, starting from 2019 contract winners will have to pay 20% tax even for projects underway.

Federal law states that the prices in the contracts cannot be negotiated and owner of the contract cannot pay more than what is mentioned in the contract. Accordingly, the cash shortfall should be made good by the service providers, i.e. contractor companies. Overall, their loss could reach USD 0.6-0.75 bn.

Author: Maria Rybina, Investment specialist

To watch...

Rusagro, Norilsk Nickel and Polymetal are due to release trading updates for Q4 2018

Sources: Rosstat, Vedomosti, Kommersant, Bloomberg, TKB Investment Partners (JSC); January 2019