The Russian equity market contracted last week in line with a global equity sell-off. The MSCI Emerging Markets and MSCI World indices fell by 1.7% and 2.8%, respectively, in US dollar terms.

Russian equities remained relatively resilient in the face of a sharp drop in oil prices. Brent crude oil fell by 11.7% in US dollar terms to below USD 60 per barrel. The drop came on the back of fears that OPEC+ might not cut production to support the supply/demand balance in the oil market. The strong fundamentals of many Russian companies and the resilience of country’s economy to external shocks supported the Russian equity market.

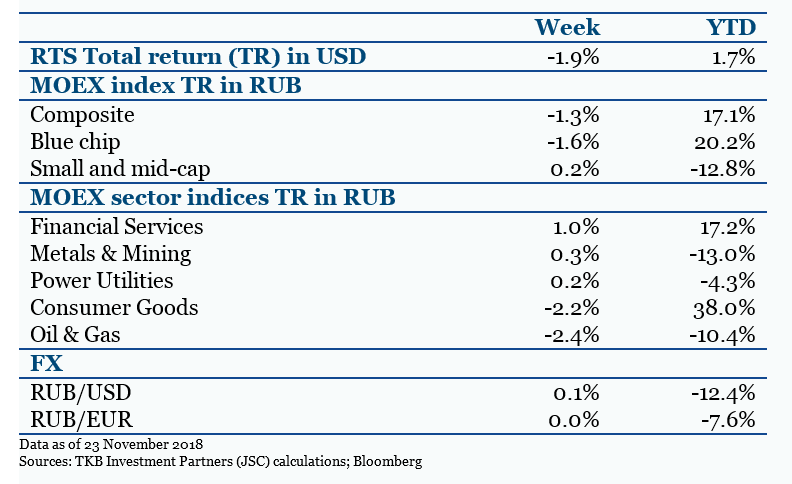

The metals and mining sector outperformed thanks to gold producer, Polyus. Its share price rose by 10.2% in rouble terms despite flat gold prices and in the absence of price-moving corporate news.

The financial services sector lagged other indices. VTB, Moscow Exchange and Sberbank were the main losers: their stocks fell by 5.3%, 2.8% and 1.0%, respectively, in rouble terms. This was effectively a correction after the gains these stocks made two weeks ago, with no news to justify the performance.

Russia’s macroeconomic indicators were mixed in October. Industrial production was boosted by stronger coal production and better output of a wide range of manufactured products. For example, metallurgic production rose by 19.6% YoY after dropping by 6.5% YoY the previous month. Electronic goods output, specifically computers, also surged by 12% YoY after contracting by 1.3% YoY in September. Retail sales growth weakened in October compared to September: non-food sales slowed amid slowdown in growth of real wages.

The head of the Central Bank of Russia (CBR), Elvira Nabiullina, gave a speech in the State Duma, in which she:

· Appealed for structural reforms, saying that monetary policy tools were proving insufficient to offset the internal constraints on the Russian economy. Reforms would allow the development of a new growth model amid external shocks, the high risk of a trade war, and capital outflows. Nonetheless, the CBR expects the Russian economy to grow by 1.5%-2% in 2018 and by 1.2%-1.7% in 2019, and to accelerate to 2%-3% by 2021

· Ms Nabiullina also confirmed that the CBR is unlikely to cut its key rate before the end of 2019. The regulator would stick to a moderately tight policy due to increasing risks of external shocks and high inflation expectations.

***

Lukoil, Aeroflot, Sberbank, Bank of St.Petersburg and RusHydro are due to publish their financial results for Q3 2018.