Russian equities rose last week in US dollar terms despite the drop in oil prices. There was positive news: the US is unlikely to impose new sanctions against Russia until 2019. The new sanctions bill had been proposed by a group of senators at the beginning of August and it was waiting for Congress approval. The delay reflects the reshuffle in the government after the mid-term elections and the tasks the senators have to agree on by the end of the year. There is also no rush: the US has found no evidence that Russia interfered in the mid-term elections.

The price of Brent crude fell by 3.5% in US dollar terms over the week. It remained under pressure amid market concerns over oversupply. Meanwhile, we think that the oil price is currently in its equilibrium range. Please read our recent flash note for more details.

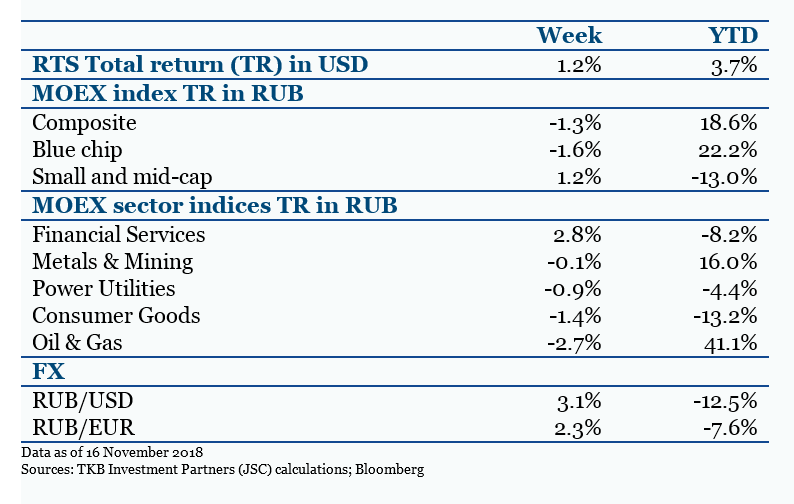

The financials sector outperformed other sectors. Moscow Exchange, VTB and Sberbank were the leaders: their stocks rose by 5.2%, 4.2% and 1.8%, respectively, in rouble terms. Moscow Exchange benefited from corporate news: it won an appeal against a previous court decision. Now the company can release the RUB 874 million that had been locked up in provisions. This could boost income and, potentially, dividends. VTB and Sberbank were likely supported by the news of a delay in new sanctions.

Oil and gas companies underperformed other sectors. Investors continued to take profits amid falling oil prices. Rosneft, Tatneft ordinary shares and Lukoil were the main detractors. Their stocks fell by 10.2%, 6.5% and 5.3%, respectively, in rouble terms.

As a part of President Vladimir Putin’s May decree, Russia should enter the top-5 of world economies by 2024, as measured by GDP per capita. To ensure that, the share of investment should reach 25% of GDP by that time, up from 21% in 2017. In the interim, economic growth should be more than 3% by 2021. It should be mostly driven by investment growth of 6%-7% per year from 2020. S&P thinks that the Russian government could fail to reach those goals. The rating agency said that investments could grow by only 3.2% per year over 2020-2021. One constrain is restricted budget expenses, which ensure macroeconomic stability. Delays in the realisation of government infrastructure projects also keep investments from growing. The potential for a surge in private investment is doubtful: it grew by only 1.3% in the first half of 2018. Low labour productivity, state dominance in business and low levels of competition are the key factors. As a result, S&P said, the economy could grow by only 1.7% in 2019-2020 and growth was unlikely to accelerate from there. To achieve higher results, Russia needs to implement judicial reform and privatisations and enhance business competition.

Bloomberg said that achieving 3% growth by 2021 would be possible, but it would not be sustainable without structural reforms. Otherwise, the sanctions would likely keep the government from reaching its goals. According to analysts, if no sanctions had been imposed since 2014, Russia’s GDP would have been 6% higher. Considering all the negative factors, such as falling oil prices, a tight monetary policy and unstable emerging markets, Russia’s GDP could have been 10% higher. Bloomberg thinks that Russia needs to boost its labour productivity to drive sustainable economic growth.

The International Energy Agency refreshed its20-year energy outlook to 2040. The world’s gas consumption could grow by 43.8% by 2040 compared to 2017. Russia could remain one of the largest gas suppliers with a more than 25% market share. For the moment, Europe is the main consumer of Russian gas, but demand is expected to decline by 16.4% over 2017-2040. Though Russia would continue meeting around 37% of Europe’s demand, Europe would no longer be its main export market. At the same time, China could become the largest gas consumer in the world. It would provide 30% of gas trading growth in the next 20 years. Russia’s largest gas producer Gazprom is aligned with the forecast: it is building a pipeline to China called “Power of Siberia” and negotiating another one – “Power of Siberia-2”. The IEA also said that liquid natural gas (LNG) would make up 60% of global gas exports by 2040. Russia’s share of overall LNG exports could reach 22% in 2040 compared to 6% in 2017.

***

Rosstat is due to publish macroeconomic figures for October.

MTS is due to publish IFRS results for Q3 2018.