Aidarkhan Zhubatkan

In today’s article will be discussed next themes:

• USA macroeconomics

• Impact of Palestine-Israel war

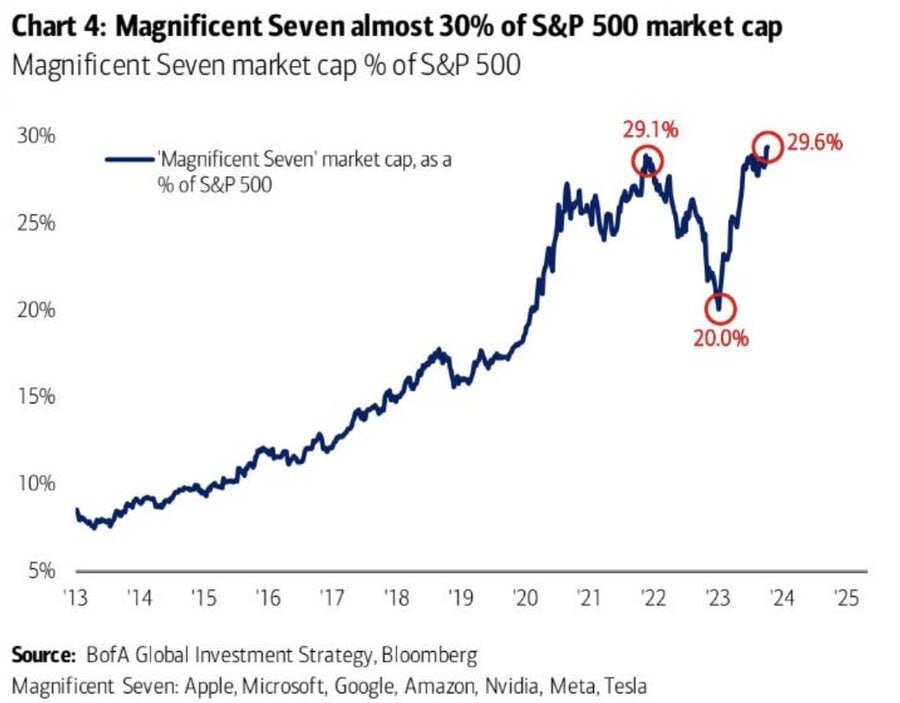

S&P500 is not about 500 companies

We used to accept S&P500, as the index of the 500 biggest market-cap companies, but shouldn’t we pay attention on what it really is? The graph below represents the proportion of “Magnificent Seven” in S&P500 composition. Seven companies (Apple, Microsoft, Google, Amazon, Nvidia, Meta, Tesla) now makes 29.7% of this composite. It doesn’t give any information about upcoming recession, but we can go deeper and find out, that 2023 rose by index was actually made by these 7 companies, while other 493 companies showed 3% increase. Unfortunately, now we can’t say, that S&P500 shows people’s belief in whole market, it’s more about that “Magnificent Seven”

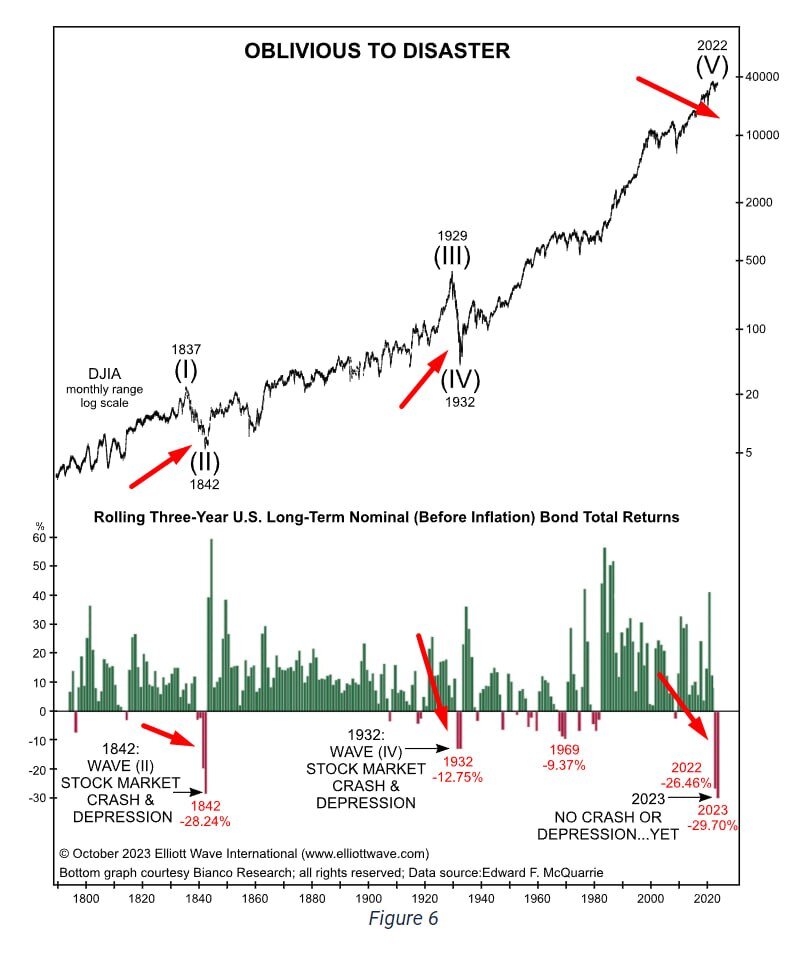

Сurrent debt market situation

The historical data show the correlation between debt market and stock market (represented by Dow Jones Industrial average). As we can see, every fail in debt market with duration more than one year consequently leads to crash on stock market. It’s only about big fails, this notice is very important. The historical data comes from late 1700s. How Robert Prechter says, it’s obvious disaster.

Thanks to President Biden

Let’s talk about some changes, that appeared during Joe Biden’s presidency. (Some ideas for Trump’s company) There are two graphs below.

First one illustrates the rise of USA sovereign credit risk. Obviously, it’s hard to imagine, as it was with Roman Empire, but getting back in May 2023, we can easily remember talks about US technical default. The difference in compounds of congress and senate makes debates more active and creates additional difficulties in regulation of budget issues as well, as credit risks.

Second statistical data is too bad to be real. The rate of withdrawal of 401K savings increased up to 4.3 in 2022 from 2.2 in 2020. What does it tell? Americans started spend their savings 2 times quicker. The reasons of that phenomena varies largely, but the main one is problem in credit payments, which can significantly impact on further sequence of bank crisis events.

Black Monday

There will be no explanations. No hard data to understand. The graph show the correlation between DJI in 1987 and Nasdaq100 in 2023 year-to-date changes. They are pretty similar, aren’t they?

The signs of upcoming danger

Here are presented two graphs, showing obvious signals for recession and market drop, as a result.First one shows the signs from leading economic index. As we can see, every time since 1960, the fall in the index was the start of recession. The last episode was in 2020, but fortunately Fed stimulated the economy in time.

Second one is about the spread between 2-years and 10-years treasures. The situation in the field of TLT is very depressive. Yet market hasn’t believed believe, that Fed is going to cut rates. It is just a matter of fact, that we will have rebounce of this spread. We can’t predict the exact date, but we know, what is going after.

Wallstreet “bullish” mood

The last theme in the US is the stock market “bullish” mood. Interesting detail: we witnessed 22 ascending gaps in 34 trading days, from July 27 to September 14, 2023. Among them were the series "4 ascending gaps from 5 trading days" and even "9 ascending gaps in 10 days”! Consequently by the end of that 34 days, index fell. It turns out that someone pulled the price of the index higher at the start of trading session and drained the volume during the trading session? Big players rules.

Destabilised Middle East and oil’s rally

There will be no illustrations, I just thought to share with my personal opinion on the topic. Nowadays, it is true, that we are on the edge of the starting war. We wait for that, no matter how pessimistic it sounds. There is US involved on the side of Israel and Iran, helping their Palestinian partners.

It’s my personal opinion based on my political view of the situation. To start with, I don’t support an aggression of any sides of the conflict. There are some consequences I am waiting for:

1. New wave of sanctions on Iran

2. Engagement of other Arabian countries

3. Oil embargo, as in 1973

4. Increase of the deficit in US budget, as there will be provided more help to Israel

5. New historical high of oil prices and hyperinflation in US

Next time, I am going to make overview of the situation in Eurozone and Germany, as well.