1. Getting to know Goldfinch

Goldfinch is a decentralized lending platform that allows anyone to be a lender, not just banks. Let's take a look at the two main beliefs on which the protocol is built:

- Investors will increasingly look for new sources of income in the context that bond rates have reached the lowest rates in history. It is becoming difficult to find new sources of income. Investors have become interested in cryptocurrency. So this is just the beginning of a new wave of investors looking for new types of returns.

- Companies are now moving in the direction of cryptocurrencies. Economic activity is becoming more and more programmable, and a new wave of investors looking for positive returns will all lead to new systems.

Customers of large companies have asked to create crypto accounts for them, these accounts are sought by both consumers and traders. They are interested in speculating on cryptocurrency, they see cryptocurrency as a safer alternative to their local currencies. So, when we have consumers who are looking for crypto accounts and traders who are also looking for accounts it inevitably follows that consumers will transact directly with these sellers.

All of this economic activity is moving down the chain, becoming more and more programmable, adding to this a new wave of investors who are looking for new sources of income. All of this will create a new system where anyone in the world can become a lender. So that not only huge banks can lend. For this to work, you need an organized mechanism. This mechanism is goldfinch, which will create this market and organize all the activities in it.

2. How is Goldfinch different from other DeFi lending protocols?

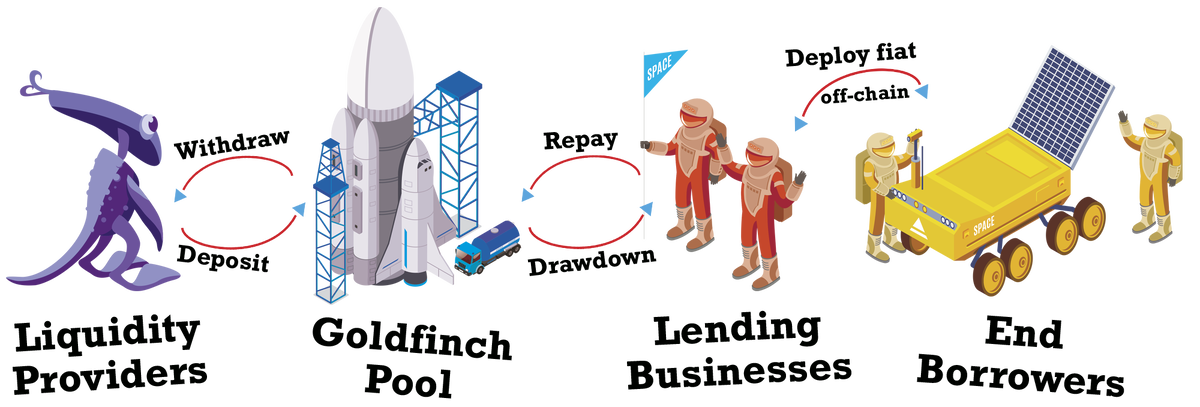

The Goldfinch project wants to unite the defi-sector with the physical world. That is, everyone can inject liquidity into pools, and their pools will lend to real enterprises from the physical sector.

How does GoldFinch Finance work?

The protocol works by extending lines of credit to lending companies. These companies use their lines of credit to obtain USDC from the pool, and then exchange them for fiat and place them in their local markets. In this way, the protocol ensures the utility of cryptocurrency - in particular, its global access to capital, leaving the actual provision and servicing of credit to the businesses best suited to do so.

On the investor side, cryptocurrency holders can make deposits into the pool to generate income. When the lending companies return their interest back in minutes, it is immediately paid out to all investors.

The main advantages and differences between Goldenfitch and other projects are:

- No loans

- Verification of solvency of the future borrower

- Possibility of participation not only of borrowers but also of companies

- Multistage process of choosing the future borrower

All this makes the project not only safe, but also highly effective and reliable for participation.

3. Key differences between the roles of Senior Pool LP and sponsor.

Goldfinch as a protocol has four main participants: sponsors, liquidity providers, auditors, and borrowers.

- Borrowers are companies that are looking for loans. They then create pools of borrowers, and these pools are evaluated by sponsors.

- Sponsors are the people who evaluate pools of borrowers, and they invest their own capital as the capital with the highest risk of "first loss" in pools of borrowers.

- Liquidity Providers - are participants as long as they invest in the pool.

- Auditors - are in charge of screening people for fraud. They vote to approve borrowers before borrowers are allowed to withdraw any capital.

How does it all work together? Let's start at the bottom, there are borrowers, now financial companies all over the world, who are looking for loans. They create a pool by saying: I want to borrow a million dollars and I'm willing to pay x%, and I want you to know the rate and the frequency of repayment, h the repayment date. With these terms, the borrowers will go to the sponsors, where they have to answer their questions. Sponsors need to know everything, since they are contributing their funds to the tier 1 tranche.

Many sponsors contribute capital to the first-order tranche, and the protocol sees that it is a reliable pool of borrowers. It starts automatically allocating capital from the second-order pool to the second-order tranche. This is where the capital is provided by the liquidity providers. Because the two tranches are full, this means that the borrower pool is full and the borrower can withdraw that capital for their needs. And then they make their payments.

Auditors act as the primary check on the borrower for fraud and other malicious activity. They vote to approve borrowers before borrowers can draw funds into the pool.

Liquidity providers and sponsors.

Sponsors ask questions directly to borrowers and decide if they want to provide capital for the junior tranche of the borrower pool. If the answer is yes, the capital is transferred to the Junior tranche, of which 10% remains for reserves in the protocol and 20% is reallocated from the Senior tranche, since the Liquidity Providers do not bear the risk of losing payments on the first loan installments. As a result, the Senior Pool receives an effective interest rate equal to 70% of the nominal interest rate on the loan.

To incentivize sponsors to provide capital early on, the protocol provides an additional token reward for all sponsors who contribute early, with the reward for subsequent sponsors decreasing as the borrower pool reaches its limit. A percentage of the reward becomes available to sponsors in proportion to the borrower's principal payments. This ensures that rewards are available only after the loan proves useful for the record.

Sponsors may enter into legal agreements with the borrowers of the agreement before capital is provided. This option is not in the protocol; sponsors will have to work directly with borrowers.

In addition, sponsors can evaluate other sponsors, which helps increase the leverage provided by the senior pool. To do this, it is sufficient to delegate GFI tokens to another sponsor.

When GFI tokens are delegated to a sponsor, they serve as collateral against possible defaults on that sponsor's positions in the borrower pools. To encourage the delegation of tokens to other sponsors, the protocol redistributes the rewards in GFI tokens in proportion to the borrowed funds and profitability of the borrower pools.

Liquidity providers, unlike sponsors, provide capital to the senior pool. The senior pool then automatically allocates this capital to the senior tranches of borrower pools in accordance with the leverage model. In this way, the senior pool provides diversification.

To compensate sponsors for possible first losses, 20% of the senior tranche's nominal share is redistributed to the junior tranche.

When liquidity providers contribute capital to the senior pool, they receive an equivalent amount of FIDUs. FIDU is an ERC-20 LP token. Liquidity providers can withdraw capital at any time by exchanging their FIDU tokens for USDC at an exchange rate based on the senior pool's asset value, less a 0.5% withdrawal fee. The exchange rate for FIDU tokens increases over time as interest from the loan is returned to the senior pool.

Sometimes it may happen that there is not enough liquidity in the senior pool to exchange FIDU to USDC, then the liquidity provider must wait for some time until there are loan repayments or funds from new liquidity providers.

To summarize, we see that sponsors may have higher yields, but they must understand borrowers and screen out bad deals. Whereas liquidity providers have lower yields than sponsors, but they remove the risk of defaulting on the first loan payments.

Official site: https://goldfinch.finance/

Module 1 Challenge:

Original blog post RU: https://zen.yandex.ru/media/id/5f605e65a4e5ea54d7774a6d/goldfinch-kriptozaimy-bez-zaloga-v-realnom-mire-ru-614e4f19777d79340b94355a

Original blog post ENG: https://zen.yandex.ru/media/id/5f605e65a4e5ea54d7774a6d/goldfinch-no-collateral-crypto-loans-in-the-real-world-eng-614e80dfca7f4571a4d47e19

Twitter thread:

1) https://twitter.com/D1eselll/status/1442183281076748301

2) https://twitter.com/D1eselll/status/1442183287183577093

3) https://twitter.com/D1eselll/status/1442183293219131396

4) https://twitter.com/D1eselll/status/1442183299464527878

5) https://twitter.com/D1eselll/status/1442183306322141184

6) https://twitter.com/D1eselll/status/1442183310168449030

7) https://twitter.com/D1eselll/status/1442183312005550083

8) https://twitter.com/D1eselll/status/1442183313976745991

Youtube video:

https://youtu.be/GePclMBEYsA

My Discord: SHLIF9570