- Money Money Money.

Herschel Walker is an athlete who signed big contracts, with both the USFL and NFL. One day, he came to me and told me he was going to invest in a fast-food franchise. I told him, “Herschel, you are a friend of mine, but if you do that, I will not speak to you again.” Because of the relationship we had (and continue to have), he decided not to make the investment. The company went bankrupt two years later. Herschel is now a wealthy man, and he thanks me every time I see him.

- No investing failure company.

If you read these financial publications for a while, you will start to pick up on the cadence and get a feel for what’s happening in the market, which funds are the best, and who the best advisers are. Stay with the winners. Often, you will read about somebody who has made money quickly and then relies on one of his friends to invest his fortune. That friend has no track record, and if it weren’t for his connection to a rich investor, he wouldn’t have any money. Beware of instant stars in the world of finance. Trust the people who do it again and again, and who are consistently ranked high by the four best institutional business media outlets. But trust your own common sense first.

- Invest according to the strategies of the winners

There are numerous firms that provide comprehensive charts and other information on the best returns from certain financial advisers and funds. Study those charts, not over the short term (maybe they just got lucky) but over a fifteen- or twenty-year period. Invest with the help of a major firm like Goldman Sachs, Morgan Stanley, Bear Stearns, or Merrill Lynch. These are your hard-earned savings at stake. Don’t take unnecessary risks. Generally there is a reason for success. When you look at legends like Alan “Ace” Greenberg and Warren Buffett and marvel at how good they are, you will likely see that what makes them so successful is the same quality you should apply to every one of your own investments—common sense. I’ve read many of Warren Buffett’s annual reports. In every case, what fascinates me is that he is able to reduce things to the simplest of terms.

- Study those charts, not over the short term but over a fifteen- or twenty-year period.

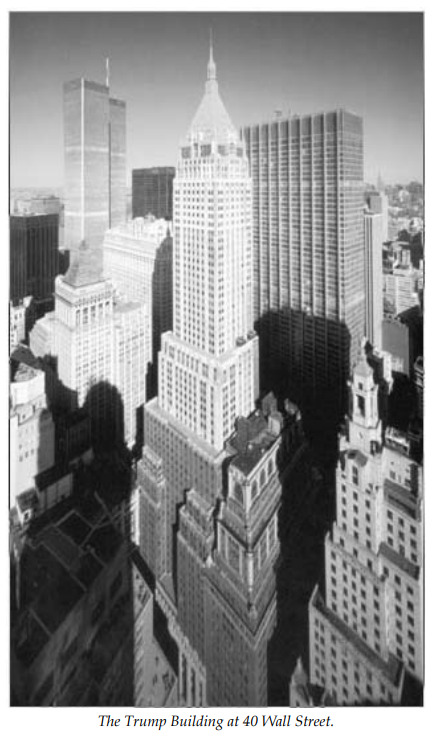

One of the best deals I ever made was the acquisition of the tallest building in lower Manhattan, a 1.3-million-square-foot landmark known as 40 Wall Street. I got it for $1 million, and the negotiation was all about timing and intuition. The next buyer was the Kinson Company, a group from Hong Kong. They made a great deal, and after the purchase was complete, I requested a meeting with them to discuss a possible partnership. They weren’t interested in a partnership, but they did want to make 40 Wall Street the downtown equivalent of Trump Tower, including a public atrium. It sounded like a beautiful idea.

- Make Profitable Deals

As you can probably guess, the Kinson group proved to be relatively clueless about renovating, running, and leasing out a New York City skyscraper. They weren’t in the real estate business to begin with—they were mostly in apparel—and they were in way over their heads. They poured tens of millions of dollars into the building but were getting nowhere. They had problems with tenants, contractors, suppliers, architects, even the owners of the land, a prominent family from Germany, the Hinnebergs. Eventually, Kinson wanted out, and they called me.

- Bad example of how not to do business

It was now 1995 and the market still wasn’t so good. Kinson had every reason to want to get out, and they wanted to do it quickly and quietly. So the negotiations began, with me offering them $1 million in addition to assuming and negotiating their liens. I also made the deal subject to a restructured ground lease with the Hinneberg family. They accepted my terms without question. Why? Because they wanted out—and fast. They knew it and I knew it, and because I knew it, the negotiation was easy. There was another crucial aspect to this deal, which proves the importance of knowing what the other side wants: All of the prior leaseholders had dealt with the agent of the Hinneberg family. The agent insisted on increasing the rent and raised other financial obstacles that he said the owner insisted upon. I had to see for myself what the Hinnebergs wanted—was it money, or something else? If you want the truth, go to the source and skip the translation by the intermediary. I flew to Germany with Bernie Diamond, my general counsel, for a face-to-face meeting with the owner, who seemed impressed by the fact that I would travel across the Atlantic to see him.

- Know what the other side of the deal wants.

- Don't use Broker Translator

A good negotiator must be flexible to be successful. When I bought 40 Wall Street, it was virtually vacant. I told the existing leasing broker, a friend of mine, that I was going to renovate the building and get tenants. I offered him the chance to be my exclusive rental agent. The broker had been the agent for the previous owners of the building, who had been having big problems getting tenants. He was so sure I would fail that he said he would take the job only if I would pay him a retainer of $60,000 per month, starting immediately. He said he would deduct his future commission from that guaranteed fee. His offer was impossible for me to accept. I owned a vacant building with existing losses, and the broker, who had been unable to produce in the past, was asking me to pay cash up front. I told the broker that his offer showed a total lack of faith in my ability to be successful—a broker getting paid without producing a tenant was unheard of. The broker remained inflexible in his position. We parted company. I hired another high-quality broker, who willingly accepted the opportunity on the usual terms—no lease, no commission. I renovated the building. The broker made millions in commissions in the next two years. The original broker’s inflexibility cost him a small fortune, plus he lost any future business from me.

- A good broker must be flexible

When I took over 40 Wall Street, my associate Abe Wallach, who orchestrated the purchase, was certain that the only viable solution was to convert the building to a residential cooperative apartment house. His reasoning made sense, given the depressed market for office tenants and the incentives the city was giving for residential development downtown. All of the real estate brokers shared his view that leasing to office tenants wasn’t feasible. They said the floor sizes were either too small or too large for renting. They complained that the lobby, elevators, and building systems required extensive renovations with questionable results. I was leery of their recommendation because the cost of residential conversion was high, plus the five floors occupied by a law firm would have to be bought out for megabucks and that would screw up any construction timetable. My instincts told me the building could become the prime office location it once had been, and that there had to be a way to make it work I asked George Ross to see whether he could devise a workable scenario, and he came up with an interesting new approach. He suggested we envision the 1.3-million-square-foot building as three separate structures on top of each other:

- The top 400,000-square-foot tower had small floors with spectacular views, and he was convinced it would quickly be rented to boutique

tenants who would pay higher rent for the prestige of being a fullfloor user on a high floor. - The middle 300,000 square feet could be rented for less per square foot, but those rents would still more than cover the purchase price and the cost of renovation.

- The bottom 400,000 square feet might be tougher to rent, but even if those floors were completely empty, the building would still be profitable, assuming our projections about renting the top 700,000 square feet were correct.

- Profitable in the actions taken

- Confidence that you are doing the right thing

Emboldened by George’s plan, I discarded the idea of residential conversion and relied on our construction expertise to turn 40 Wall Street into a successful office building. We redesigned and modernized the lobby and building systems, and when the rental market improved, we were ready. Now, the building is worth hundreds of times what I paid for it. I guess my instincts were right.

- Modernization of a building for resale

If you’re careful about what you reveal, you’ll have more flexibility as you gather more information about the contours of the deal. In order to complete Trump Tower as I envisioned it, it was necessary for me to control an adjoining site on Fifty-seventh Street owned by Leonard Kandell and leased to Bonwit Teller, a dying department store chain. Len Kandell was a shrewd real estate developer whose ultimate desire was to own land in strategic locations forever. I tried to gain a longterm lease, but Kandell was asking for too much in rent, and we were stalled. Meanwhile, during negotiations to buy air rights from the adjoining Tiffany store, which would allow me to build a larger Trump Tower, I learned that Tiffany also had an option to buy the Kandell property at a fair market price. This was news to me, and a crucial piece of information, but I didn’t let anyone know how important that news was to me. I led Tiffany to believe I was interested only in air rights, without calling any special attention to their option to buy the Kandell property. They sold me their air rights and basically threw in the option as part of the deal. Then I told Len Kandell that I was no longer interested in a lease on the land. I was going to buy it, using the Tiffany option.

- Hide your intentions until the end

Kandell didn’t want to sell, and I really didn’t want to buy. With my new leverage, I suggested reconsideration of a long-term lease. This time, Kandell agreed, and we quickly closed on a mutually acceptable lease, beginning a friendship that continues to flourish with his heirs. Don’t be confined by your expectations. Sometimes, what we think we want and what we actually want are two different things. On more than several occasions, I have discovered in the middle of negotiations that what I had wanted was the wrong thing. Sometimes, my negotiating partners have given me ideas I hadn’t thought of. Even adversaries have given me new ideas. Sometimes, a big question suddenly comes into my mind and I begin to think in a new direction. Cut yourself some slack. It’s okay to change your mind and suggest a different approach—as long as you haven’t made any commitments to the other side. Some people, while admitting I’m a good negotiator, have said I’m devious. I’m too busy to be devious. I just assimilate new information quickly and move forward in unexpected ways—unexpected to the other party as well as to myself. That’s one reason I find negotiating exciting. Perhaps because I’m a Gemini, I believe there is a duality to negotiating. You have to balance reason with passion. Reason keeps you open. Passion keeps your adrenaline going.

- Sometimes, what we think we want and what we actually want are two different things

- I just assimilate new information quickly and move forward in unexpected ways

Before you begin any negotiation, write down your objectives. Then try to anticipate what the other side might want. Find a way of talking nabout the deal and setting up parameters that will keep either of you from getting locked into an impossible position. Know what you want, bottom line, but keep it to yourself until a strategically necessary moment. Once all of the issues are on the table, you’ll have a better approach to navigating your way to your desired solution.

- Know what you want, bottom line

Know that your negotiating partner might bluff, too. But when it comes to serious endeavors, you don’t want bluffers of any sort. Study the person’s history. I’m always surprised when newcomers to the real estate industry think that talking big and fast will get them somewhere with me. Construction of a big building is painstaking work and that’s the kind of person I want doing it—someone who will take the time to do it right. I don’t want people who think they can get it done in record time. That can spell disaster.I remember one contractor who tried every angle to convince me how fast he was. His time estimates were so far off that I couldn’t take him seriously, but I let him keep trying to pitch me just to find out how full of it he really was. He must have thought he caught me on a bad day or with my guard down, but my guard wasn’t down—I was just incredulous. Finally, I told the guy that what he was saying was exactly what I never wanted to hear. He was the first person whose bid was ruled out.

- Impossible get it done in record time

My first big deal, in 1974, involved the old Commodore Hotel site near Grand Central Station on Forty-second Street in New York City. The hotel was vacant, except for a sleazy club called Plato’s Retreat and some rundown street-level stores. The land was owned by the Penn Central Railroad, which was bankrupt and owed New York City $15 million in back taxes that the city desperately needed. The city was about to default on its bonds, and banks would not consider real estate loans in Manhattan. My idea was to transform the Commodore into a state-of-the-art hotel. I had a six-point plan:

1. Buy the land from the railroad.

2. Induce the railroad to use the purchase price to pay the City of New York the back taxes it owed.

3. Convince a New York State agency with the power of eminent domain to accept a deed to the land to condemn all existing leases.

4. Persuade the city to accept a fixed rental and a share of the profits in lieu of taxes.

5. Find a big hotel operator to join me in the project, since I had no hotel experience.

6. Convince a bank to loan me $80 million to build the hotel.

When I first told my lawyer, George Ross, of my plans, he told me I was crazy to attempt something so bold in such a bad economic environment. I told him I was determined to get it done. He agreed to help.

For two years, I stuck to my guns. Eventually, it paid off. The railroad sold me the land for $12 million and used the money to pay the city its back taxes. The Urban Development Corporation accepted the deed to the land and agreed to condemn all existing leases, provided I would pay all damages to the displaced tenants. The city agreed to the lease from UDC with a fixed rent and a share of the profits. Hyatt became my partner in the deal and funded half of it. I got a loan from the Bowery Savings Bank to cover the cost of acquisition and construction. The hotel became the Grand Hyatt. The fact that I was stubborn and had achieved a result others deemed impossible jump-started my career as a developer.

- Know that your idea can pay off

15 I like to move quickly, but if a situation requires patience, I will be patient. The speed depends on the circumstances, and I keep my objective in mind at all times. This alone can be a patience pill. I’ve spent from five minutes to fifteen years waiting for a deal. One good tactic for speeding up a deal is to show a lack of interest in it. This will often make the other side rekindle their efforts to get something going. I was very interested in a deal once, but I had a hunch that it wasn’t a good idea to look too eager to these people. I would put off their calls and do my best to appear aloof. Then I said I’d be traveling for a couple of weeks and would get back to them after that. While I was “traveling,” they used the time to modify their position and present to me almost precisely what I’d been hoping to get. It saved us all a lot of negotiating time. A good tactic for slowing down a deal is to distract the other side. One way is to drop hints about whether a certain aspect of the deal should be looked into further, or to mention other deals and properties as examples. That will set them off in a direction that consumes their time and focus. While they’re off on a tangent, you’ll still be on target. One time, I was in the middle of a negotiation that seemed to be speeding out of my control. I suddenly asked the other side if they knew the history of a particular development, implying that their understanding of it might be crucial. They figured the development must have had some bearing on what we were trying to accomplish together, so they backed up a bit, took some time to investigate it, and gave me control of the negotiations with enough time to assess everything at my leisure. I got the upper hand.

- enough time to assess

16 In 1999, I began construction on the tallest residential tower in the world, Trump World Tower at the United Nations Plaza. The location was terrific—the East Side of Manhattan, close to the United Nations, with both river views and city views. It was hot stuff, but not everyone was happy about it, especially some diplomats at the United Nations, who didn’t want their thirty-eight-story building to be outclassed by our ninety-story tower. According to CNN, UN secretary general Kofi Annan acknowledged talking with New York City mayor Rudolph Giuliani about the project and how to stop it. “It will not fit here,” the Ukrainian ambassador, Volodymyr Yel’chenko, told CNN, “because it overshadows the United Nations complex.” When the protests became vocal, I used my own brand of diplomacy and refused to say anything critical of the United Nations. I predicted that many ambassadors and UN officials would end up buying apartments in the building. Sure enough, they have. But as soon as we were in business, the city hit us with an enormous tax assessment, costing us over $100 million more than we thought we should pay. We decided to take the only action possible. We sued the city for $500 million. For four years, we fought this case. The city lawyers held their ground, and we held ours. We could have given up. It’s not easy to take on the

- Don't Lose , It is strategically important to win

For many years I’ve said that if someone screws you, screw them back. I once made the mistake of saying that in front of a group of twenty priests who were in a larger audience of two thousand people. I took some heat for that. One of them said, “My son, we thought you were a much nicer person.” I responded, “Father, I have great respect for you. You’ll get to heaven. I probably won’t, but to be honest, as long as we’re on the earth, I really have to live by my principles.” When somebody hurts you, just go after them as viciously and as violently as you can. Like it says in the Bible, an eye for an eye. Be paranoid. I know this observation doesn’t make any of us sound very good, but let’s face the fact that it’s possible that even your best friend wants to steal your spouse and your money. As I say every week in The Apprentice, it’s a jungle out there. We’re worse than lions—at least they do it for food. We do it for the thrill of the hunt. Recently, I’ve become a bit more mellow about retribution and paranoia. Although I still believe both are necessary, I now realize that vengeance can waste a lot of time better spent on new developments and deals, and even on building a better personal life. If you can easily dismiss a negative from your life, it’s better to do so. Seeing creeps as a form of corruption that you’re better off without is a great time-saving device. Still, sometimes you’ve just got to screw them back.

- don't waste your time on useless people

- better spent on new developments and deals, and even on building a better personal life.