_ Jurij C. Kofner, non-residential research fellow, Skolkovo Institute for Emerging Markets Studies; editor-in-chief, analytical media “Eurasian Studies”. First published on: Vienna Institute for Security Policy. Munich, 18 December 2019.*

Being first and foremost an economic integration bloc, arguably the Eurasian Economic Union’s (EAEU) most important aim is to create a single interior market for goods. Over the last five years, from the signing of the Union treaty in 2014 up until 2018, to which extent has the EAEU been successful in achieving this objective?

The new EAEU customs code

The Eurasian Economic Union began its journey as the EurAsEC customs union in 2010 with its own supranational customs code. At the beginning of 2018 it was finally replaced with the new EAEU customs code. It is a comprehensive codified international treaty, during the preparation of which an audit of all previously concluded international treaties governing customs legal relations was conducted, the existing order and technology of customs operations were rethought, approaches to the use of information technologies in the implementation of such operations were changed.

The new code provides for a number of innovations: electronic customs declarations, automatic transactions, shortening the time of release of goods to four hours at most, the institution of “authorized economic operators”, and a single-window mechanism. A large list of competencies was transferred from the national customs administration to the Eurasian Economic Commission (EEC). About 70% of the proposals received from the business communities were taken into account when preparing the new customs legislation.

Common tariffs regime, but with exemptions

Average trade weighted tariffs of the EAEU have decreased over the years, yet are still rather high – at 5.6% comprehensive, 11.5% for agricultural products and 4.7% for non-agricultural products (Table 1). For comparison, the trade weighted average tariffs of the EU are only 3.0%, for agricultural products – 8.1%, and for non-agricultural products – 2.7%.

A number of significant exceptions remain from the existing tariffs regime concerning goods released for the free circulation in Armenia, Kyrgyzstan and Kazakhstan at lower import customs duties compared to EAEU rates. In case of Armenia and Kyrgyzstan, which upon their ascension have received a phasing-in period until 2025, imported goods can be freely traded subject to surcharges up to the amount of duties calculated at EAEU rates. In case of Kazakhstan, which has lower import duties due to its separate WTO obligations, the sale of such goods is permissible only within the country itself. Furthermore, certain exemptions for categories of goods are outlined in Article 29 of the Union Treaty.

Box 1. No sweet exemption

For the past three years, sugar production in the countries of the Eurasian Economic Union has exceeded consumption. In 2018, almost 7 mln tons of sugar were produced while domestic consumption totaled only 6.8 mln tons. For 2019, the surplus of 650 thousand tons is estimated. In this regard, sugar was qualified as a “sensitive good”, on which the Union’s member states make decisions at the level of the EEC Council. In order to provide equal conditions so that domestic sugar could compete with cheaper foreign sugar, the EAEU countries agreed to impose import duties. However, despite this, Kazakhstan, which already enjoys exemptions for the import of foreign sugar, additionally bypasses the EAEU’s import tariffs by importing sugar from Ukraine and Europe duty-free through its special economic zones. Afterwards it reexports this sugar to the rest of the EAEU single market in the form of confectionery products and non-alcoholic beverages. By doing so, it violates the Union’s equal competition conditions. At a meeting of the Eurasian Intergovernmental Council (EIGC) in April 2019 the parties agreed that from 2020 on Nursultan will discontinue this practice.

Intra-Union trade

Quantification of the impacts of the introduction of the customs union is complicated by the fact that Eurasian integration has coincided with business cycle effects – the impact of the 2008-2009 recession and the crisis triggered by the collapse of the oil prices at the end of 2014. A recent analysis, conducted by the Vienna Institute for International Economic Studies (wiiw)[1], shows that the early stages of Eurasian integration following the establishment of the EurAsEC custom union were associated with generally positive average trade creation effects on the member states. According to the study, the member states de facto traded much higher relative to the levels predicted and relative to a hypothetical no-integration scenario. However, the positive effects largely dissipated towards 2015 due largely to the above-mentioned fall in oil prices and a recession in Russia made worse by international sanctions.

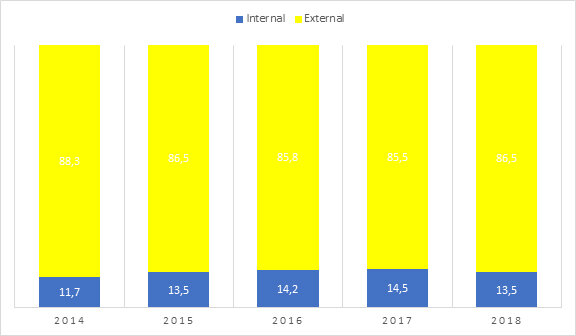

From 2015 to 2018 intra-EAEU trade increased again by 23.6%, which, however, is still 5.4% lower than it was in 2014 (Table 2). More importantly, during this period the EAEU hasn’t been able to increase intra-Union mutual trade in relation to trade with third parties. From 2014 to 2018 the former remained at 13.5% in average as compared to 86.5% in average of the latter (Chart 1, Table 3)

Chart 1. EAEU trade turnover structure (internal vs. external, in %, 2014-2018)

Source: Table 3.

Sanctions and trade policy disputes

Despite the relatively well functioning of the customs union, albeit with some of the above-mentioned exemptions, a major and often criticized obstruction to the free movement of goods in the EAEU is the absence of a truly unified trade policy. Firstly, quite periodically trade disputes arise between the Union member states. These most often concern sanitary and phytosanitary measures (Box 4), but also the bypassing of customs duties (Box 1 above) and trade remedies (Box 2). The disagreements are made more acute due to the structural similarity of the economies of the member states and due to a strong influence of private business interests on state policy in the post-Soviet countries.

Box 2. Anti-dumping measures on EU herbicides

The Eurasian Intergovernmental Council in early 2019 agreed to lift the Kazakhstani veto on the EEC Board’s anti-dumping measures directed against herbicide producers and plant protection products from the European Union. Earlier, Kazakhstan did not want to adopt the EEC’s measures. Russia’s chemical industry had the prime interest in pursuing the anti-dumping measures. Nursultan, on the other hand, was interested that Kazakhstani farmers could buy better and more economical herbicides from Germany and other European countries. Now Kazakhstan has agreed with the decision of the Eurasian Commission, and anti-dumping measures may come into force. This decision can serve as a precedent that member states should respect the results of the EEC’s anti-dumping investigations. At the same time, in order to prevent similar disagreements in the future, it would be important to ensure greater precision and transparency in such investigations.

Secondly, the EAEU’s skewed trade policy is by and large a result of unilateral Russian measures against Western countries. In 2014, in response to sanctions imposed by the United States, the EU, Canada, Australia, Ukraine, Norway and various Balkan states, Russia introduced retaliatory import bans on food products originating from these countries. Additionally, in 2016 Moscow banned the transit of goods through its territory to and from Ukraine (Box 3).

Box 3. Ukrainian transit

Russian countersanctions, particularly the 2016 ban on the transit of Ukrainian goods to Kazakhstan and Kyrgyzstan through the territory of the Russian Federation, have always been one of the main arguments against the sincerity of Eurasian integration. Ukraine, Kazakhstan and Kyrgyzstan have repeatedly urged Moscow to lift its restrictions. Kiev applied to the World Trade Organization (WTO) to investigate the legality of the Russian authorities’ actions. In early April 2019 Ukraine lost the dispute. The WTO Arbitration Group, which investigated the complaint made by the Ukrainian side, came to the unprecedented conclusion that the Russian Federation had neither violated the General Agreement on Tariffs and Trade (GATT), nor the WTO accession document, as it had the right to impose such restrictions for reasons of national security.

In light of this, it is quite significant that on the eve of the Eurasian Intergovernmental Council later the same month, the Russian government announced that “after consideration of the official appeal” by Nursultan and Bishkek, the Russian Federation decided to “allow transit traffic through its territory to Kazakhstan and Kyrgyzstan of a list of priority industrial goods from Ukraine”.

However, the problem has not been resolved completely. Now Kazakhstan and Kyrgyzstan are accusing Russia of de-facto quoting coal exports to Ukraine. Indeed, they now are able to supply their coal in transit through Russia, however only with special permits. Yet, the Ministry of Economic Development of the Russian Federation is constantly permitting the volume of transit lower than that requested by Bishkek and Nursultan.

Thus, Russia has had to ensure unilateral application of restrictions, including controlling the flow of sanctioned products through EAEU partner countries. After Belarus and Kazakhstan blocked Russian proposals in EAEU bodies for closer customs cooperation on the movement of embargoed foods, mobile groups consisting of Russian customs officers, border guards, police, and Federal Service for Veterinary and Phytosanitary Surveillance (Rosselkhoznadzor) inspectors began patrolling areas bordering Belarus and Kazakhstan. This development undermined the EAEU’s objective of removing controls on the movement of goods at internal borders. Moreover, systematic control at internal borders was largely ineffective at combating massive reexports of sanctioned products. The estimated total cost of embargoed food reexported to Russia through Belarus from August 2014 to the end of 2016 was $ 2.7 billion[2]. Russian systems detected less than 1% of the actual volume of products reexported via Belarus[3].

In order to return to a truly common trade policy, there now are three options. Firstly, Russia might decide to lift its food import bans. This might be done either unilaterally, as with case for transit to and from Ukraine, or in response to a lifting of sanctions by the Western international community. With the current deadlock from both sides over Crimea and eastern Ukraine this scenario seems rather unlikely. Secondly, Moscow therefore continues to agitate other member states to join Russia’s countersanction policy. E.g., at the end of June 2019, the EEC’s minister for trade Veronika Nikishina mentioned discussions on introducing collective sanctions against third countries in response to restrictions imposed on one of the member states[4].

Since this seems no more likely than the first scenario, the third and current development is aimed at increasing the effectiveness of the de-facto two-tier customs control, i.e. for embargoed goods and for the rest of imports. The Commission and the member states have introduced plans to ensure this through the application of a digital “goods traceability system” that is currently being formed, including the signing of a corresponding agreement in February 2018. As part of this initiative the plan is to trace the import, reexport, transit and circulation of an increasing assortment of imported products and transit goods by marking them with control (identification) marks and digital tracking seals. Furthermore, in early 2019 Rosselkhoznadzor stated that Belarussian authorities have agreed to cease the certification of sanctioned fruit and vegetable products originating from third countries in transit through Belarus[5]. However, there remain technical difficulties of how to effectively trace food products (e.g. tomato imports). And most importantly, it will be very difficult to harmonize the separate national digital tracing systems, such as the Russian “Merkury” system, since they are run by private business interests. This is likely to create another difficult-to-overcome barrier to the functioning of the internal market. In the end, this development of creating a two-tier customs control still does not solve the problem of the EAEU’s inconsistent trade policy.

Conclusion

So, five years after its inception in 2014, was the Eurasian Economic Union able to create a single domestic goods market? The short answer is “yes, but” there remain numerous barriers, exemptions and restrictions to the free movement of goods.

Between 2015 and 2018 intra-EAEU trade in goods increased by more than 1/5 and there have been visible trade creation effects early on. Moreover, in 2018 the EAEU received a modern customs code. However, these relative successes were offset by persisting tariff exemptions and ongoing trade disputes between the member states, as well as by Russian unilateral countersanctions. These issues de-facto created a two-tier customs union and skewed the Union’s trade policy. More importantly, there was no increase in the share of intra-EAEU trade relative to the Union’s trade with the rest of the world, which remain at a 1 to 7 and a 6 to 7 ratio, respectively. Currently much effort is being put into establishing a digital “goods traceability system”, which, despite being an original initiative, might not solve the underlying problem and even cause new barriers.

Progress in this respect could be ensured by implementing the following actions over the next five years: 1. by strengthening the Commission’s competencies, funding and manpower; 2. by supporting and accelerating intergovernmental consultations between the relevant national authorities; 3. by enhancing the role of the EAEU Court and giving it more powers; 4. by a generally greater effort of the member states towards ensuring liberalization and market competition.

Notes:

[1] Adarov A. (2019). Trade effects of Eurasian economic integration. In: wiiw Monthly Report 2019/04.

[2] Yeliseyeu A. (2019). The Eurasian Economic Union: expectations, challenges and achievements. GMF.

[3] Yeliseyeu A. (2017). Belarusian shrimps, anyone? How EU food products make their way to Russia through Belarus. GLOBSEC Policy Institute.

[4] RIA News (2019). The EAEU may begin to impose sanctions against third countries. (In Russian). // https://ria.ru/20190626/1555936362.html

[5] Reform (2019). Belarus stops re-export of sanctioned fruits and vegetables from third countries to Russia. (In Russian). // https://reform.by/belarus-prekrashhaet-rejeksport-sankcionnyh-fruktov-i-ovoshhej-iz-tretih-stran-v-rossiju/

Source: http://greater-europe.org/