Tax payments have a significant impact on the operations of SibDalRegion LLC. This organization applies the general taxation regime. In this regard, it calculates and pays to the budget the following taxes: value added tax, property tax, corporate income tax, insurance premiums and transport tax, and is also a tax agent for personal income tax.

Let's proceed to the calculation of the tax burden of SibDalRegion LLC.

The category "tax burden" can be interpreted differently. Some experts consider the concepts of "tax burden" and "tax burden" different and suggest differentiating them.

The tax burden is understood as both the relations between business entities and the state on payment of mandatory tax payments and the value reflecting the potential impact of the state on the economy through tax mechanisms. The tax burden acts as an indicator characterizing the actual level of impact.

Other researchers, bringing their contribution to the development of economic science, offer their own interpretation of the concept of tax burden.

For example, V.R. Yurchenko defines the tax burden as a share of withdrawal of part of an economic entity's income to the budget system and extra-budgetary funds in the form of taxes and fees, as well as other tax payments.

Another researcher, I.N. Danina, on the basis of systematization and assessment of existing approaches to the definition of the tax burden defines it as the degree of influence of the current system of taxation on the financial condition, nature and incentives for the development of enterprises.

The most controversial problem in this area is the problem of calculating the tax burden at the level of the economic entity. In Russian science and practice there is no unified approach to this indicator.

The analysis of existing points of view on this problem allows us to focus on the following aspects. The majority of scientists suggest not to include the personal income tax in the calculation of the tax burden on the organization, since the organization acts as a tax agent in this case. The second key aspect is which taxes and levies (indirect taxes) should be included in the calculation of the tax burden of the organization. The third point is the indicator to which the absolute tax burden should be related. As such, scientists consider revenue, value added and newly created value.

To get a fuller picture of the tax burden of SibDalRegion LLC, we will use different methods of calculating the tax burden of enterprises.

Calculation of the load in accordance with the methodology of the Department of Tax Policy of the Ministry of Finance of the Russian Federation:

According to the explanatory note to the financial statements for 2016, the taxes paid in 2016 amounted to:

Income tax: RUB 6,565,870.00.

VAT: RUB 24,530,720.80.

Transport tax: 26,051.00 RUB.

Property tax on legal entities: 86,649.00 RUB.

Total for 2016: RUR 31,209,291 (31,209,291)

N 2016= (31,209.291 / (123,239 + 749 + 6,236))*100%=24.0%

According to the explanatory note to the 2015 financial statements, taxes paid in 2015 were equal to those paid:

- property tax 122,535 rubles,

-Transport tax 32,400 rubles,

-Taxation 52,038,853 rubles,

-payment for the negative impact of 166 rubles,

Income tax - profit tax 4,422,241 rubles.

Total for 2015: 56,616,195 rubles.

NN 2015 = (57,810,730 / (280,498 + 470+40,383))*100%=17.6%

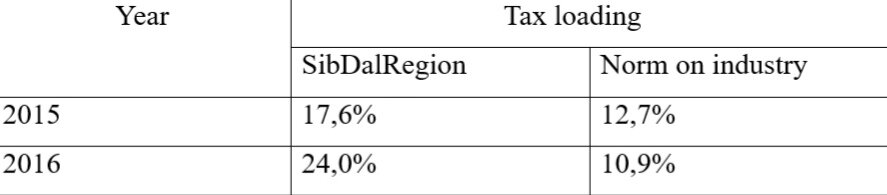

Tax burden standard (type of activity - construction) according to the Federal Tax Service website:

In 2015, the tax burden (type of activity - construction) was calculated according to the data of the website of the Federal Tax Service:12,7%

In 2016..: 10,9%

Let's summarize the obtained data in Table.

Comparing the standard indicators and calculated indicators of the tax burden of SibDalRegion LLC, we can conclude that the tax burden of the organization exceeds the standard indicators in 2015 and 2016. This means that the organization overpays taxes, i.e. reserves for optimizing the tax burden.

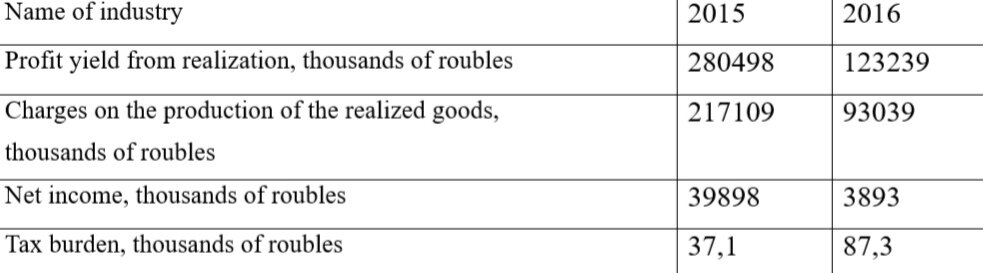

The results of calculations based on the methodology for determining the tax burden developed by M.N. Kreynina are given in the table below.

Based on the results obtained, we can conclude that in 2016, the tax burden was 87 kopecks per rouble of the balance sheet profit or the share of taxes in the balance sheet profit was 87.3%. The growth of this indicator to the value of 2015 was 50.2%.

Based on the analysis of the tax burden, in order to reduce the tax burden and improve the financial condition of the company, the management of SibDalRegion LLC can recommend the measures presented in the next chapter.