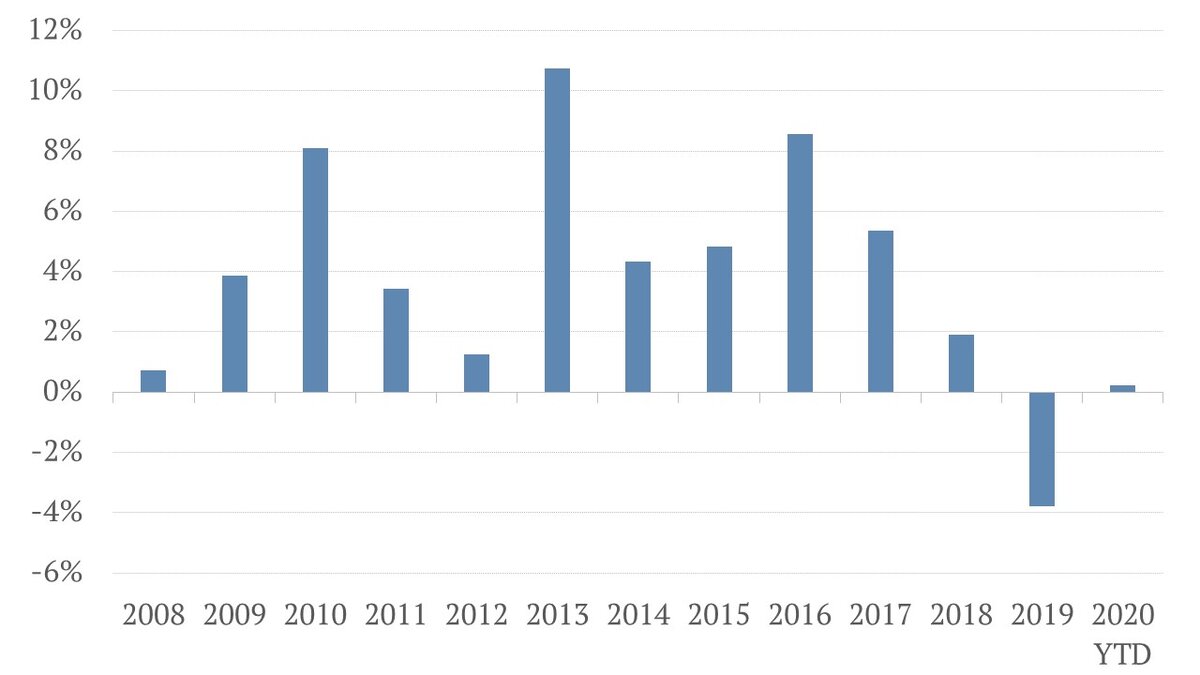

BNP Paribas Russia Equity fund and VanEck Vectors Russia ETF are the largest funds in their categories. Their assets under management each total slightly more than USD 1 billion. Each calendar year from 2008 to 2018, BNP Paribas Russia Equity outperformed VanEck Vectors Russia ETF[1]. In 2019, for the first time in both funds’ history, the ETF outperformed the equity fund over a full calendar year. Was this a sign of a systematic deterioration in the fund investment team’s[2] ability to capture mispriced stocks on the Russia equity market?

Excess return of BNP Paribas Russia Equity fund over VanEck Russia ETF (in USD terms, net of fees)

Note: Both funds were launched in spring 2007; for institutional share class of BNP Paribas Russia Equity fund

Source: Bloomberg, TKB Investment Partners; Data as at 18 September 2020

Past performance is not indicative of future performance

“Usual suspects” for bad performance are not relevant

Portfolio manager. Norges Bank Investment Management manages the largest sovereign wealth fund in the world with assets of more than USD 1 trillion. Part of this portfolio has been managed by various external managers for 20 years. Norges Bank Investment Management terminated one of its mandates with an external asset manager after two weeks. They did so because the portfolio manager responsible for their mandate left the asset management company[3].

The key person for BNP Paribas Russia equity fund performance is Vladimir Tsuprov. He has been the lead investment advisor for the fund since its inception in February 2007. Vladimir still remains in this role.

Investment team. There were changes to the team in 2019 and 2020. Were they crucial? The team retained its top rating for pillar “Team” from Morningstar in its Analyst Rating assessment.

Morningstar wrote in its fund reports:

- “One of the best-resourced, most experienced teams” November 2018

- “One of the best-resourced and most-experienced teams in the category” August 2019

- “We continue to hold TKB’s investment team in high regard. Positive aspects include experience, overall tenure at the firm, dedication to the Russian equity market, and the local presence in St Petersburg, which gives the team an edge, in our view.” August 2020.

Investment process. There were no crucial changes to the investment process during 2019-2020. The investment process also retained its top score for pillar “Process” from Morningstar.

Morningstar wrote in its fund reports:

- “Fundamental research is the core of this effective and thorough process” November 2018

- “A strong fundamental bottom-up process” August 2019

- “The thorough and well-structured approach has been executed in a disciplined fashion, earning it a Process rating of Above Average” August 2020.

So, the problem is not with the team or the process. Perhaps the team made mistakes in its views on the investment cases of companies?

Key detractors from the excess return in 2019: Norilsk Nickel and the ordinary shares of Surgutneftegas.

These two positions detracted around 600bp from the fund vs. the ETF’s excess return in 2019[4]:

- 5% underweight in Norilsk Nickel. The stock price rose by 89% mainly on the back of a 31% rise in its commodities basket price. This was mainly due to palladium prices rising by 55% (all figures in in USD terms)

- 4% underweight in Surgutneftegas ordinary shares. Surgutneftegas’s ordinary shares rose by 116% in USD terms. This was mainly due to rumours: 1) In August, that the company may start to use its USD 50 billion cash reserves to buy its ordinary shares; 2) In October, that the company was planning to purchase a stake in Lukoil. These rumours were unconfirmed by any reliable source.

Can we consider these two positions as mistakes by the fund investment team? We do not think so.

Norilsk Nickel. The strong rise of the company commodities basket was an unlikely event. At the end of 2018, the probability of Norilsk Nickel’s commodities basket price rising by no less than 31% over 2019 was 4%[5]. We rarely make strong out-of-consensus calls on a particular commodity price change as we do not consider ourselves experts in commodities price predictions.

From a company-specific perspective, ESG issues have for many years put pressure on the fair price of the company, in our view. Was it fair to punish the company’s valuation for ESG issues? At the end of May 2020, there was a material environmental accident – 21 000 tonnes of fuel oil spilled into a river, which resulted in Norilsk Nickel being fined USD 2 billion. The company’s stock price subsequently underperformed the market, dropping by 16% in June vs. a fall of 2% for the market (all figures in USD terms).

Surgutneftegas ordinary shares. We do not make investment decisions based on speculative rumours. We check the credibility of stories. If there is evidence that a particular rumour is genuine and important, we include it in the investment case of a company. We did not find this to be so with the rumours about Surgutneftegas. We kept the underweight in the stock. In 2020, Surgutneftegas’s ordinary shares underperformed the market as the speculative demand faded way. The fund’s underweight has led to a positive contribution to the excess return vs the ETF from the start of 2020 to 18 September 2020.

Does this mean the investment team made no errors in 2019? No.

The largest misjudgment was the overweight position in diamond producer, Alrosa, whose stock suffered from lower diamond prices in 2019. This detracted around 100bp from the fund vs the ETF’s excess return. The situation is different from the position with Norilsk Nickel as we should have been more cautious in our projections of Alrosa’s business at the end of 2018: 1) In retrospect, diamond prices in 2018 appear to have been higher than the cyclical average; 2) In our projections, we failed to take account of the favourable gem mix in 2018. We later adjusted our model and saw an upside potential in Alrosa’s stock, so we have kept it in our portfolio, although now it is not an overweight position.

Authors: Egor Kiselev, Head of International Business & Investment Marketing; Marina Tsutskiridze, Junior Investment Specialist

[1]. For institutional share class of the BNP Paribas Russia equity fund

[2]. Investment team of TKB Investment Partners has been advising the fund since its inception in 2007

[3]. From “Investing with external managers” Page 124

[4]. We used Bloomberg’s PORT function for the performance attribution analysis for BNP Paribas Russia Equity vs. VanEck Russia ETF

[5]. We used Bloomberg’s scenario analysis function to calculate this probability